A decade-long legal battle, $30 billion on the line, the top two major payment network companies, and numerous merchants sounds like a plot for an interesting legal drama!

As they say, "Fact is stranger than fiction," and in this case, the reality is that a court battle concerning "swipe fees" is raging between US merchants and two of the biggest credit card companies in the world, Visa and Mastercard. The proposed settlement by the two credit card corporations was worth a startling $30 billion and was viewed as a resolution to the dispute. This settlement provided some comfort to merchants, who have often expressed their worries about the exorbitant costs associated with credit card transactions. However, according to recent developments, a federal judge has rejected the proposal. This means that Visa and Mastercard have no choice but to make more adjustments to address the merchants and their concerns.

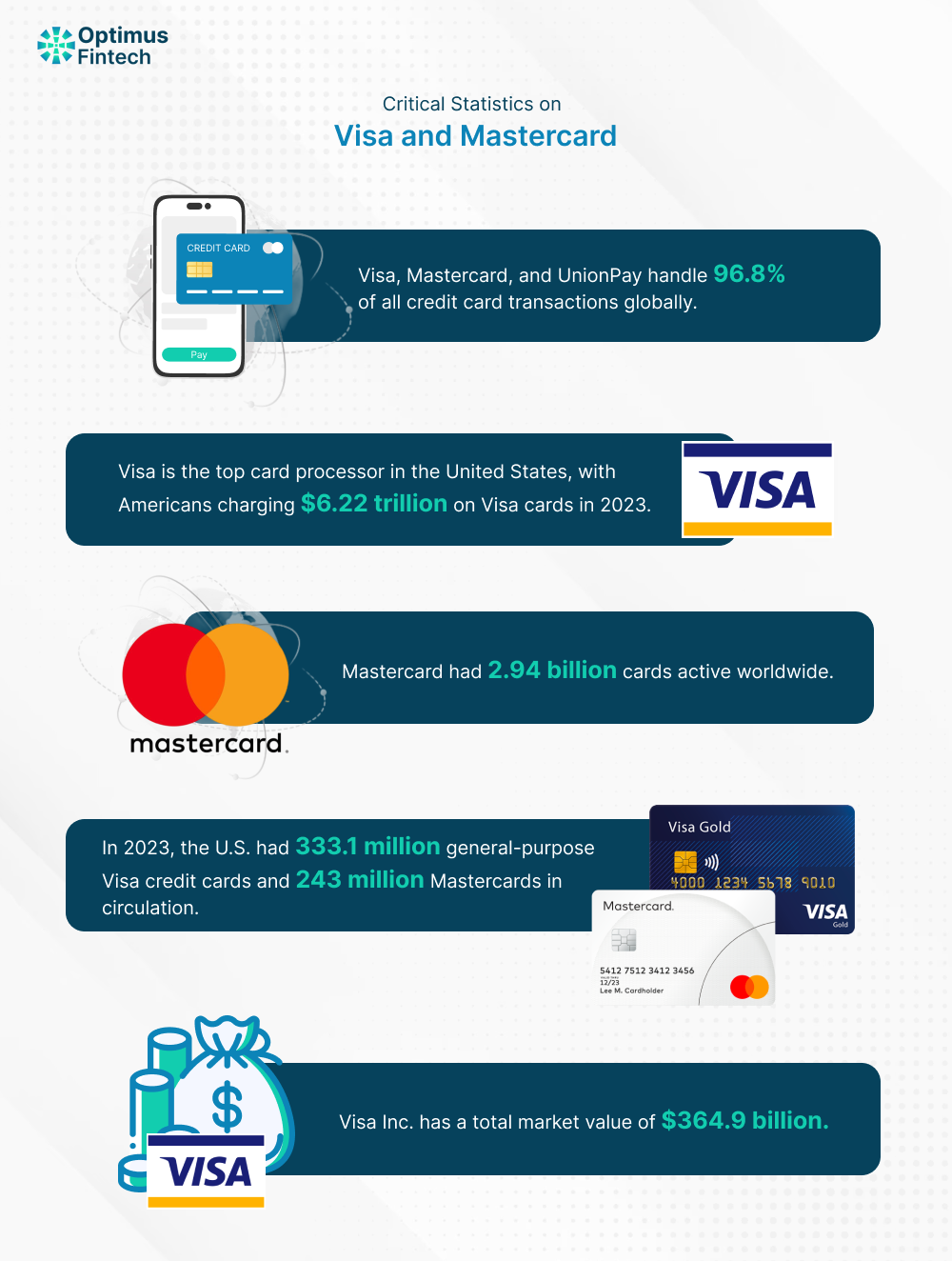

Before we get into the details of this controversial settlement, let’s have a look at some of the statistics of credit card giants in the industry. Currently, Visa, Mastercard, and UnionPay manage 96.8% of all credit card transactions that take place on a global scale. Continuing their dominance, Mastercard has 2.94 billion cards active worldwide, while Visa Inc. has an aggregate market value of $364.9 billion! It is safe to say that when a $30 billion settlement is proposed by these industry giants, it is bound to create drama in the financial market.

History of the Settlement

The roots of this settlement trace back to a long-standing antitrust class-action lawsuit filed in 2005. According to the lawsuit, the merchants accused Visa and Mastercard, along with the banks that issue their cards, of working closely to inflate interchange fees. These fees typically range between 2% and 4% of the total transaction and can add up greatly, especially for small businesses with minimal profit margins. The proposed settlement promised to lower those fees by at least 0.04% percentage points for a minimum of three years. The lawsuit argued that these inflated fees were the result of anti-competitive practices, including the prevention of diverting customers toward less expensive payment methods.

While there have been many legal cases making the rounds, this case has definitely become one of the biggest antitrust class-action lawsuits in U.S. history. The only other case that came close to this was in 2012, valued at $7.25 billion, but it was also rejected by several large retailers. They believed that the deal was not addressing the core issues.

Why was the Settlement Rejected?

While there are multiple reasons behind the rejection of the settlement, one of the primary reasons is that the agreement did not resolve the problems of the merchants involved. The U.S. District Judge in this case, Margo Brodie, stated in her ruling that she was “not likely to grant final approval.”

While Judge Brodie’s statement has not been fully disclosed to the public, she seems adamant about not granting the approval until major changes and negotiations are done to help the merchant class.

The rejection of the $30 billion settlement has left those involved in a rut. The credit card giants now have no other option but to renegotiate the terms and conditions of the settlement, or they will have to head back to court. This rejection was a huge victory for the large retailers who revolted against the settlement. They argued that Visa and Mastercard would continue to rule over the masses on their own terms while blocking the competition in the market.

What is the Current Situation?

As of now, the situation has not been publicly addressed ever since the federal judge rejected the proposed settlement. This simply means that the terms and conditions for swipe fees will continue to remain the same. Additionally, in the proposed 2024 settlement, Visa and Mastercard agreed to a series of negotiations aimed at addressing merchants' concerns.

The key points of the settlement included the following:

- Maintaining swipe fee rates as of December 31, 2023, for a five-year period.

- Remove certain anti-competitive regulations that had previously stopped merchants from directing customers to lower-cost payment solutions.

- Allow merchants to apply surcharges to customers based on the type of credit card they used, perhaps reducing the costs associated with increased swipe fees for premium rewards cards.

Despite the fact that the proposed settlement offered some relief, it had mixed reactions from the merchant community. More than 90% of the merchants who were in favor of the settlement were small businesses. Though the negotiation seemed unsatisfactory, they were compelled to gain even the smallest amount of benefits that were on offer. However, trade groups that represented big retailers, such as the Merchants Payments Coalition (MPC) and the Retail Industry Leaders Association (RILA), did not sit quietly. They were vocal with their thoughts and revolted that the settlement did not address the imbalance in the payment ecosystem.

Christopher Jones, an executive committee member of the MPC, stated that the proposed settlement would have allowed credit card firms to "keep price-fixing swipe fees and blocking competition. Thankfully, the judge made the right call in recognizing what a bad deal this would have been for Main Street merchants and their customers."

What Does It Mean for Merchants?

For merchants, the rejection of the settlement is both a challenge and an opportunity.

On one hand, the skepticism surrounding the 2024 settlement means that the ongoing legal battle could go on for months or even years. This will strip the merchants of the already minimal benefits that the settlement would have provided. While this is concerning for merchants, the stakes are even higher for small businesses, who are struggling with the rise in costs and thin profit margins. While not ideal, the settlement offered a temporary solution to reduce the immediate financial strain on these businesses.

On the other hand, the rejection of the proposed settlement also opens the opportunity to gain a better, more beneficial deal down the line. Big retailers, who have been the most vocal against the settlement, argue that the proposal does not address the root causes of the high swipe fees. By rooting for a better deal, these retailers hope to receive better negotiations from Visa and Mastercard. These include lower fees, more flexibility in payment processing, and greater transparency in how fees are finalized.

Merchants are currently in a state of uncertainty, with no obvious solution in sight. The next steps in the case will likely involve further negotiations between the parties, with the possibility of a new settlement proposal being put forward. However, it is also possible that the case could go back to court, where a judge or jury would ultimately decide the outcome.

What Lies Ahead

As the case progresses, merchants will need to carefully consider their alternatives and balance the urgent need for relief with the possibility of a better settlement in the days to come. Meanwhile, Visa and Mastercard will have to make further adjustments amidst the rejection of the settlement to bring the decade-long dispute to an end.

Ultimately, the decision of this lawsuit will have serious implications for the future of the payments sector in the United States, especially for the millions of businesses that depend on credit card transactions to process payments from customers.