Imagine you're reviewing your business's monthly financial statements, and suddenly, a list of fees catches your eye each one with a name that seems more complicated than the last. As you dig deeper, you realize these aren't just numbers; they represent costs that directly impact your bottom line. But what are they really? Why are they there, and how do they affect your business? Understanding the different types of fees in the payment reconciliation process is like decoding a secret language. This blog post will help you break down those fees, so you can better manage your finances and keep your business running smoothly. Let’s Explore!

1. Transaction Fees: The Cost of Doing Business

Any payment you process, whether through online payment systems, debit cards, or credit cards, incurs a transaction fee. Payment processors charge these fees in exchange for facilitating the transaction. Although they typically vary from 1% to 3% each transaction, they can accumulate, especially when dealing with big volumes.

Why this matters: Your profit margins may suffer if you're not properly accounting for transaction fees. To guarantee the accuracy of your books, these fees must be meticulously matched with the appropriate payments throughout the reconciliation process.

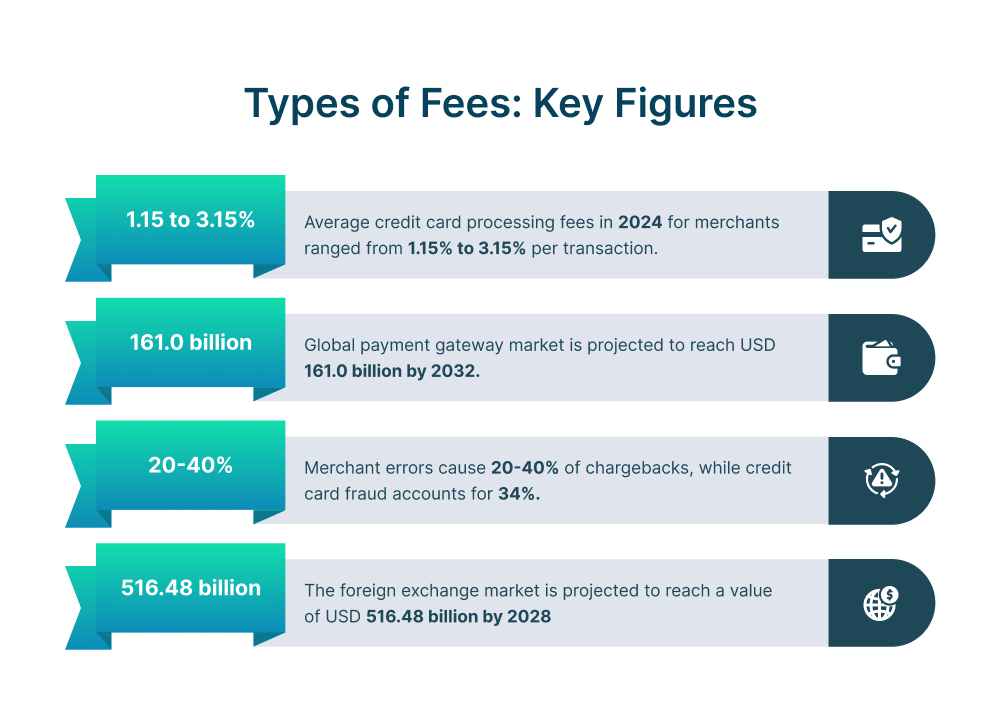

Statistics: In 2024, the average credit card processing fees for merchants ranged from 1.15% to 3.15% per transaction. However, the actual fee can vary on the terms set by credit card companies, but also on the merchant category code, or MCC, of the business involved.

2. Gateway Fees: The Digital Toll booth

Payment gateways serve as digital toll booths, linking your website or POS system to the payment processor. You are charged a gateway fee to process online payments, which is often charged monthly or per transaction.

Why it matters: Gateway fees are sometimes overlooked because they are combined with other expenses. To gain a thorough picture of your payment processing costs, separate these fees during reconciliation.

Statistics: By 2032, the global payment gateway market is projected to reach USD 161.0 billion, with hosted (payment service provider's payment page) and non-hosted (payments via API or HTTP) revenues reaching USD 94.99 billion and USD 66.01 billion, respectively.

3. Chargeback Fees: The Price of Disputes

The transaction is usually reversed and becomes a chargeback once a customer disputes a particular charge on their credit card. Even though it could seem like a straightforward return, the procedure might be difficult and expensive. Most card processors impose a fee, which can range from $15 to $100 per dispute, to handle chargebacks.

Why it matters: Because chargebacks cost you extra money on top of the purchase, they can significantly affect your profit margins. With reconciliation's help, you can monitor these incidents, identify patterns, and take steps to lessen them.

Statistics: Merchant errors contribute to 20-40% of chargebacks, while credit card fraud, including unknown or fraudulent purchases, accounts for 34%. Additionally, chargebacks due to stolen credit cards make up around 30% of cases.

4. Currency Conversion Fees: The Cost of Global Business

Currency conversion fees are something you will have to deal with if your firm serves clients from other countries. When a transaction includes exchanging one currency for another, these costs are assessed. Typically, they comprise 1% to 4% of the total transaction value.

Why it matters: If you're analyzing the profitability of international sales, it's crucial to account for these fees individually during reconciliation. If you don't, your financial situation may appear distorted.

Statistics: The foreign exchange market is projected to reach a value of USD 516.48 billion, with a compound annual growth rate (CAGR) of 10.31% over the next five years. In 2024, the market is expected to experience year-over-year growth in conversions, with Europe estimated to contribute 43% to the global market's growth during the forecast period.

5. Interchange Fees: The Backbone of Card Payments

Whenever a customer pays with a credit or debit card, an interchange fee is deducted from the total transaction amount. These fees are paid to the card-issuing bank and are typically a percentage of the transaction plus a fixed amount. Interchange fees compensate the bank for handling risks, such as fraud and non-payment, associated with processing card payments. The rates can differ based on the type of card used, the transaction method (e.g., in-person or online), and the industry category.

Why this matters: Interchange fees are often the most significant component of your overall payment processing costs. Understanding these fees is essential for accurate financial forecasting and ensuring that your business is not overpaying during the reconciliation of payment process.

Statistics: In March 2024, Mastercard and Visa reached a $30 billion court settlement with U.S. merchants to lower and cap swipe fees, reflecting a significant shift in their fee structures. However, it's worth noting that this settlement, if approved, would only result in a reduction of their interchange fees by 0.04% over a span of three years.

6. Assessment Fees: The Evaluation of Financial Performance

Assessment fees are charges imposed by payment processors or financial institutions to evaluate and manage the performance of your account. These fees are typically levied periodically—monthly, quarterly, or annually—and are meant to cover the cost of account maintenance, analysis, and additional services provided. While they might seem like a minor expense, they can add up over time, especially if your account is subject to frequent evaluations.

Why this matters: Regularly reviewing and understanding these fees is crucial, as they can affect your overall financial performance and budgeting. By keeping track of assessment fees, you can better manage your expenses and make informed decisions about whether to stay with your current service provider or seek alternatives.

Statistics: Mastercard plans to raise its Acquirer Brand Volume Fee, also known as an assessment fee, from 0.13% to 0.14% starting April 15. With Mastercard processing $2.591 trillion in transactions during fiscal 2023, this increase would add $259.1 million annually.

7. Network Fees: The Hidden Costs Behind Payment Processing

When you process payments through various networks, whether it's online payment systems, debit cards, or credit cards, you're often faced with network fees. These fees are charged by the payment networks for routing the transaction and ensuring it reaches the right place. While they might seem like just another cost, they can significantly impact your overall expenses, especially when dealing with high transaction volumes.

Why this matters: Network fees, though sometimes small on a per-transaction basis, can add up over time. If not properly tracked and managed, these costs can erode your profit margins. To keep your financials accurate, it's essential to closely monitor and reconcile these fees with your payment records.

Statistics: In 2024, network fees typically ranged from 0.1% to 0.5% per transaction. The exact fee can vary based on the payment network and the specific agreements you have in place with them.

Surcharges: Extra Costs on Your Bill

Surcharges are additional fees that may be added to the base transaction fee, often to cover specific costs like credit card processing or other administrative expenses. They can be a fixed amount or a percentage of the transaction.

Why this matters: Surcharges can significantly impact the total cost of a transaction, and understanding them helps in managing expenses more effectively. Properly accounting for surcharges ensures that all costs are factored into your financial planning and reconciliation processes.

Statistics: In some regions, surcharges can add an extra 1% to 4% to the transaction amount, depending on the payment method and service provider.

Tips for Smooth Fee Reconciliation

1. Transition: Transitioning from summary-level to transaction-level fee management offers a more precise view of financial operations. Transaction-level management allows for detailed analysis, uncovering insights and pinpointing discrepancies. This enhances fee tracking, optimization, and decision-making, leading to greater transparency and more effective financial management.

2.Automation: Investing in automation for fee management boosts accuracy and efficiency by swiftly processing data, reducing errors, and saving time. Automated systems track fees in real time, spot discrepancies, and refine fee structures, enhancing financial planning and decision-making. This reduces costs, improves compliance, and optimizes resource use, strengthening the financial position and competitive edge of businesses.

3.Regularly Review Fee Structures: Conduct regular reviews of fee structures on a weekly, monthly, or quarterly basis to ensure alignment with financial goals and market conditions. This process involves analyzing fee performance, identifying trends, and assessing the impact of any changes or anomalies. By systematically evaluating fee structures at these intervals, organizations can make data-driven adjustments, optimize pricing strategies, and maintain competitiveness while ensuring compliance with regulatory requirements.

4.Scheduling: Establishing daily schedules for transaction-level fee reconciliation is critical for maintaining financial accuracy and operational integrity. This practice involves systematically verifying and matching each transaction's fee data against corresponding records to promptly identify and resolve discrepancies. By performing reconciliation on a daily basis, organizations can ensure that fee assessments are accurate, financial statements are up-to-date, and potential issues are addressed before they escalate.

5.Collaboration: Establish and maintain continuous collaboration with payment ecosystem partners to enhance operational efficiency and ensure seamless transaction processing. This involves setting up structured communication channels, defining clear protocols for data sharing, and implementing real-time monitoring of transactions and fee settlements. Regular interactions with partners allow for the early identification of discrepancies, the timely resolution of issues, and the optimization of fee structures.

Conclusion

Understanding the various fees involved in payments is crucial to maintaining your company's financial stability. These costs aren't just numbers on a ledger—they directly impact your bottom line. By tracking and incorporating them into your routine reconciliation process, you ensure that your financial records are accurate and your business remains profitable. Think of it as a blend of initiative, knowledge, and organization. Initiative drives you to stay on top of these expenses, knowledge helps you understand and anticipate them, and organization ensures nothing slips through the cracks. Together, these qualities enable you to manage your money more effectively and keep your business financially healthy. So, next time you’re reviewing your fees, remember: they’re not just costs—they’re key factors in your business’s financial success.