I have been in fintech long enough to watch the same conversation repeat. CFOs call processors for better rates. Processors shuffle fees. Everyone signs another contract.

Except something fundamental changed. The thing about working in payments is you see patterns others miss; reconciliation taking weeks, fraud blocking customers, routing defaulting to whoever you contracted with instead of who's cheapest.

But the past 18 months have been different. I have watched something shift from theoretical to practical, from 'interesting idea' to 'companies are doing this and seeing massive results.'

The Invisible Leak

Money leaks constantly from payment systems. We are processing over $10 trillion in global digital payments, growing 15% annually. And most companies pay 1.5 to 2.2% of every transaction in fees to processors with zero incentive to optimize for you.

Processing $100 million annually means $1.5-2.2 million leaving yearly. Your processor profits from those fees. The networks won't volunteer savings. This is finance's most comfortable inefficiency; profitable for intermediaries, invisible to everyone else.

As payment volumes scale, fraud losses are accelerating. The EBA and ECB reported total payment fraud reached €4.2 billion in 2024, a 17% increase over the previous year, primarily driven by fraudulent credit transfers. The faster you scale, the more expensive payment infrastructure becomes, unless you do something deliberately different.

When AI Became More Valuable Than Negotiating

For years, the answer to 'how do we pay less?' was: get a better contract. Negotiate with processors. You'd negotiate slightly better rates and call it a win. Meanwhile, you were still using routing logic from 2015.

Around 2023-2024, I started seeing companies deploy AI-based payment routing. Not as a test. As actual infrastructure. The numbers were different. 26%, 50%, sometimes higher.

The same pattern appeared everywhere. This wasn't a fluke. This was structural.

The fundamental insight is simple: instead of one contract with one processor at one fee rate, what if every transaction could be routed to the optimal processor at that exact moment? That's not a small optimization. That's a category shift.

How This Actually Works

It's algorithmic decision-making at machine speed applied to a problem humans have solved inefficiently for decades. The system ingests real-time data on your transaction mix, understands fee schedules of multiple processors, monitors network conditions, and makes routing decisions for every transaction. Based on what's optimal right now.

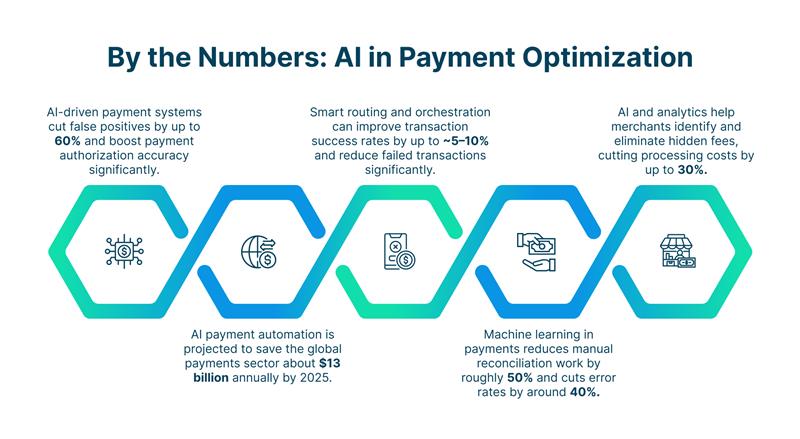

AI-driven reconciliation automation reduces manual work by 70%, and intelligent routing delivers nearly 55% savings on merchant fees. Adyen ran a pilot with 20+ enterprises, eBay, 24 Hour Fitness, Microsoft. Using AI-powered routing, the average company reduced costs by 26%. One enterprise cut payment costs by more than 50%.

I spent years in consulting saying companies could negotiate their way to 5-10% savings. One of those companies just saved 50% with algorithmic routing. That's the gap.

Beyond Routing

Payment reconciliation is expensive, lots of manual work, lots of errors. AI automates this to 80% faster AP processing and 50% reduction in days sales outstanding. That's material cash flow improvement.

Then there's fraud. The biggest blind spot: companies lose more money to false declines than actual fraud. AI fraud systems catch more fraud (50%+ loss reduction) but reduce false declines by 40%. That's $40 billion in annual merchant losses from legitimate transactions being blocked.

Companies deploying AI routing see 12-25% cost reduction and 15% improvement in approval rates. More successful transactions means more revenue. Lower costs means better margins. They reinforce each other.

What the Incumbents Are Doing

The most telling part of any trend is what institutions with the most to lose decide to do. JPMorgan Chase and Mastercard aren't experimenting for fun.

JPMorgan Chase integrated AI across payment operations and reports 30% reduction in servicing costs and 10% reduction in operational headcount. That's structural reorganization.

Mastercard's AI systems catch 300% more fraud while protecting 159 billion transactions annually. Orders-of-magnitude change.

AI and automation can reduce payment processing costs by up to 60 % and significantly cut manual workload in reconciliation tasks.When JPMorgan and Mastercard both reach the same conclusion, you are watching an industry standard being established.

The Convergence

We are at a pivotal inflection point in financial technology where three independent forces have aligned simultaneously to rewrite the rules of transaction processing.

First, payment margins have compressed to the point that traditional pricing arbitrage is no longer viable; algorithmic routing across multiple processors is now the only sustainable path forward.

Second, AI-based models for real-time transaction routing are no longer theoretical, they are production-ready and delivering measurable results.

Third, for the first time, the industry has access to real-time transaction data at scale, providing the fuel these systems need to learn and improve.

Market analysts project the financial services AI market will reach $192.7 billion by 2034, growing at roughly 22 % annually, underscoring the strategic shift underway. The future of financial operations will be defined by intelligent, dynamic routing and automation.

If your company remains tied to a single processor, rigid contracts, and manual reconciliation workflows, you are already behind a category shift whose technology is proven and whose incumbents have signaled commitment.

The question now is simple: What is your company’s move?