A colleague of mine was in Brooklyn last month and overheard an interesting exchange at a coffee shop. A CFO of a global merchant company was speaking with a Wall Street banker, visibly frustrated. “You told me our fees would be 2.6%, but we are paying significantly more than that. We are dealing with monthly minimums, unexpected assessment charges, and after a few chargebacks last month, our effective rate jumped again. What’s actually going on here?”

That got me thinking. This conversation happens thousands of times every week. Business owners believe they understand their payment costs. They see the headline rate and assume that’s the full picture. They are often wrong.

The truth? Interchange is just the opening act.

The Interchange Illusion

Most merchants think: "I pay interchange, the card networks take their cut, and that's the total cost." Wrong. U.S. merchants are paying about 2.5% to 3.5% of each transaction for all-in processing costs. But that single percentage doesn't come from one place.

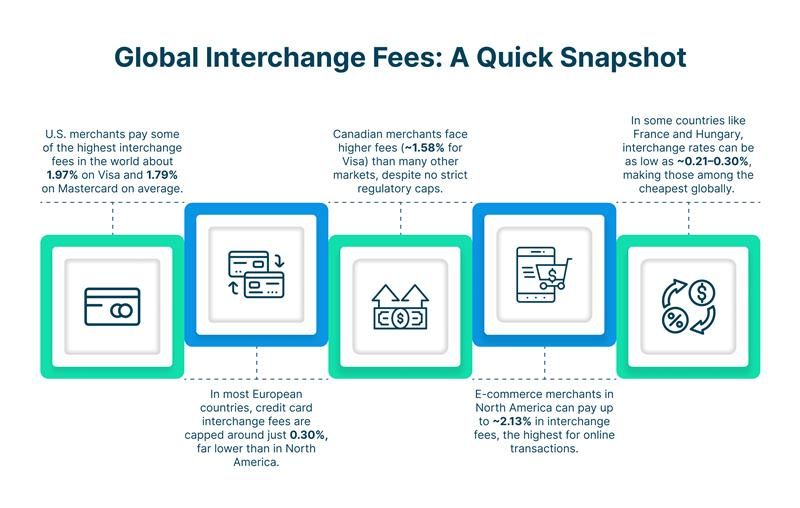

Interchange ranges from 0.5% on regulated debit to over 2% for premium credit cards, plus per-transaction fees. Visa and Mastercard control this. You can't negotiate it. But it's not the real villain.

The Real Players Have Your Money

Network Fees: Network fees, also known as interchange fees or card network charges, are transaction costs imposed by card networks like Visa, Mastercard, RuPay, or American Express. Each time a card transaction occurs, these charges typically comprising interchange, assessment, and processor markup are applied by the card networks

Processor Markup: Payment processor markup ranges from 0.25% to 0.75% on top of everything else. They route transactions, assume risk, and take their cut. Platforms such as Square, Stripe, or PayPal bundle this into rates of 2.2% to 3% plus per-transaction fees.

Chargebacks: The Profit Killer: A customer disputes a charge. You lose the money and pay a fee. Chargeback fees range between $15-$100 per dispute.On a $20 transaction, you could lose $100. But here is what hurts more, in 2025, every dollar lost to fraud costs U.S. merchants $4.61, a 37% increase since 2020. You lose the product, shipping, labor, and reputation.

Fraud Prevention Costs: You need tools to catch fraud before it happens. Software subscriptions. AI-powered detection. Address verification. Each costs money. AI fraud detection can reduce fraud detection costs by 30%. But you pay for it upfront.

Compliance and Security: The Federal Reserve's 2025 report shows fraud losses were 17.6 basis points in 2023, or $17.63 per $10,000 in transaction value, up from 7.8 basis points in 2011. What's worse? Merchants paid for 49.9% of debit card fraud in 2023, up from 46.9% in 2021. Banks paid only 28.3%, down from 33.4%. Security audits, training, and infrastructure updates are non-negotiable costs.

Global chargeback volume is projected to reach 337 million transactions by 2026, up from 238 million in 2023. Worldwide chargeback losses will climb from $33.79 billion in 2025 to $41.69 billion in 2028. Roughly 61% of chargebacks are caused by cardholders themselves, even when the transaction was valid, friendly fraud. Buyer's remorse drives 65.3% of these cases. People aren't getting scammed, they are claiming they were.

The Real Math

You are a mid-size ecommerce business processing $50,000 monthly in credit cards. Your processor says 2.6%. That's $1,300 per month.

Add network fees (0.35% = $175). Add processor markup (0.50% = $250). You are now at $1,725 monthly, that's 3.45%, not 2.6%.

Then you have two chargebacks at $150-$200 in fees, plus fraud losses at $4.61 per dollar. Suddenly $50,000 in revenue is down $2,000 in payment costs alone.

Over a year? You are hemorrhaging $24,000 to $30,000.

Online Costs More

Card-not-present payments now make up 63% of merchants' transactions. They carry higher fraud rates and higher costs. That's why smart merchants steer customers toward ACH or bank transfer, often 1.0%–2.0% versus 3%+ for cards.

The average chargeback costs merchants $190 per dispute, including transaction value, shipping, bank fees, labor, and reputation damage. For low-margin businesses, this adds up fast.

Path Forward

Know your effective rate. If it's above 3%, something's wrong. Negotiate. If you are doing hundreds of thousands yearly, ask for interchange-plus or cost-plus pricing. This can drop costs by 30–80 basis points.

Optimize for cheaper payment methods. Debit can be under 1% effective cost, versus 3%+ for premium cards. Offer ACH. Make alternatives visible.

Merchants implementing strong fraud controls and proactive refunds have seen significant improvements in dispute prevention. Prevention costs less than chargebacks.

The Bottom Line

Your payment costs are a cocktail of fees almost nobody explains clearly. Interchange gets the blame because it's visible and regulated. But it's not the main culprit. Your processor, networks, chargebacks, and fraud are eating more profit than you think.

Start reading statements line by line. Know your effective rate. Push back on fees. Everything except interchange is negotiable.