The intersection of cryptocurrency and traditional banking has never been simple, and recent revelations by Coinbase further underscore the complexities. Coinbase, a leading crypto exchange, has exposed over 20 instances where the Federal Deposit Insurance Corporation (FDIC) sent advisories to banks, encouraging them to pause or limit crypto-related services.

This move has sparked discussions about the agency’s stance on cryptocurrency and raised questions about the broader regulatory environment. So, are we seeing the resurgence of ‘Operation Chokepoint 2.0,’ a regulatory suppression strategy aimed at limiting access to financial services in the crypto world?

Let’s find out!

Unpacking Coinbase’s Findings

Coinbase’s Chief Legal Officer, Paul Grewal, revealed that the company obtained 23 documents via Freedom of Information Act (FOIA) requests. These documents detail letters from the FDIC to banks, urging them to exercise caution when dealing with crypto services. Although the full content of these letters remains undisclosed, summaries highlight concerns around consumer protection, regulatory compliance, and financial stability. The letters, dated between March and October 2022, were addressed to top bank officials; however, the FDIC did not disclose the names of the banks involved. Coinbase perceives this as an attempt to 'cut off financial access' to legitimate crypto businesses, a claim Grewal emphasized in a recent post on X (formerly Twitter).

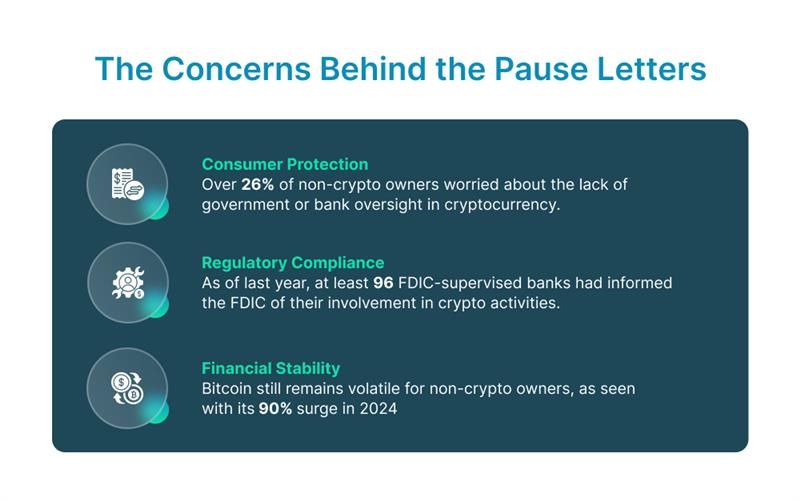

The Concerns Behind the ‘Pause Letters’

The FDIC’s cautious approach toward crypto largely revolves around a few key concerns:

- Consumer Protection: Over 26% of non-crypto owners worry about the lack of government or bank oversight in cryptocurrency, citing concerns about fraud, market instability, and inadequate consumer protection due to its inherent volatility.

- Regulatory Compliance: As of January 2023, at least 96 FDIC-supervised banks had informed the FDIC of their involvement in crypto activities, raising concerns about whether they can manage these services while complying with existing regulations.

- Financial Stability: Concerns are rising about financial stability if traditional banks offer crypto services without proper oversight. Cryptocurrencies, such as Bitcoin, remain volatile, as seen with its 90% surge in 2024 driven by demand for U.S. ETFs and favorable interest rates, heightening market instability concerns.

While these concerns are legitimate, questions arise whether they’re also being used to stymie innovation in the crypto space.

Is This Operation Chokepoint 2.0?

Originally, 'Operation Chokepoint' referred to a government initiative aimed at restricting financial services access to certain industries. 'Operation Chokepoint 2.0' suggests that regulators may now be attempting to curb the growth of crypto by restricting its integration into the banking system. Grewal contends that the FDIC’s efforts represent a contemporary chokepoint unfairly targeting the crypto industry, despite recent strides towards regulatory legitimacy.

Coinbase Pushes for Transparency

Coinbase’s push for transparency highlights a broader issue: as digital currencies become more integrated into mainstream finance, clear and consistent regulations are crucial. Grewal argues that the public deserves clarity on regulatory motives and actions. He has committed to pursuing greater transparency through FOIA and other means, stressing that the crypto industry needs an open regulatory dialogue rather than decisions 'behind a bureaucratic curtain.'

Bank Reconciliation for Banks: Implications in a Crypto World

In the context of crypto services, integrating bank reconciliation could become even more complex. For instance, if banks offer crypto services, ensuring accurate and timely reconciliation of transactions will be essential due to the rapid transaction speeds and volatility of digital assets. The FDIC’s 'pause letters' reflect an underlying concern about whether banks are equipped to reconcile these transactions, which could impact their compliance and overall stability. This cautious approach may signal a need for additional safeguards in bank reconciliation when dealing with crypto.

Payment Reconciliation for Banks: Addressing Transparency Concerns

While banks ensure that all payments match between accounts through payment reconciliation, they could face unique challenges in a crypto-integrated banking environment. As Coinbase and other crypto exchanges push for more transparency, there’s a growing demand for reconciliation practices that are both efficient and adaptable to the fast-paced world of crypto. With the FDIC urging banks to 'pause' on crypto services, some may wonder if traditional banking infrastructure is fully prepared for payment reconciliation involving digital assets. If not adequately addressed, these challenges could compromise the operational clarity that both banks and consumers expect, making it difficult to gain full visibility over transaction flows.

The Future of Crypto-Friendly Banking in the U.S.

Coinbase now stands at the forefront of the crypto industry’s regulatory battle. The company has indicated that it’s willing to work with either party following the U.S. presidential election, as both Vice President Kamala Harris and the recently elected Republican nominee Donald Trump have shown support for the crypto sector. This bipartisan shift towards crypto acceptance marks a significant departure from previous years when the industry often faced political skepticism. However, the FDIC’s caution suggests that crypto-friendly banking won’t emerge without obstacles, especially if federal regulators maintain a stance of caution.

Are Crypto Banks in Danger?

The FDIC’s position signals a broader trend among regulators worldwide to treat crypto with caution if not resistance. As more developments arise, U.S. crypto companies such as Coinbase may need to navigate an unpredictable regulatory landscape. Until clear and crypto-supportive policies are established, crypto companies may find it challenging to secure the level of banking integration they seek.

Conclusion: A Call for Balanced Regulation

The debate over crypto regulation is intricate and multifaceted. Coinbase’s recent FOIA findings reveal how regulatory caution may unintentionally limit financial sector innovation. For the U.S. to remain a leader in fintech, a balanced regulatory approach that addresses legitimate concerns without stifling innovation is essential. As the FDIC’s actions continue to evolve, open communication between regulators and the industry will play a pivotal role in shaping the future of crypto in America, especially when it comes to reconciling financial operations such as bank and payment reconciliation for an increasingly digital era.