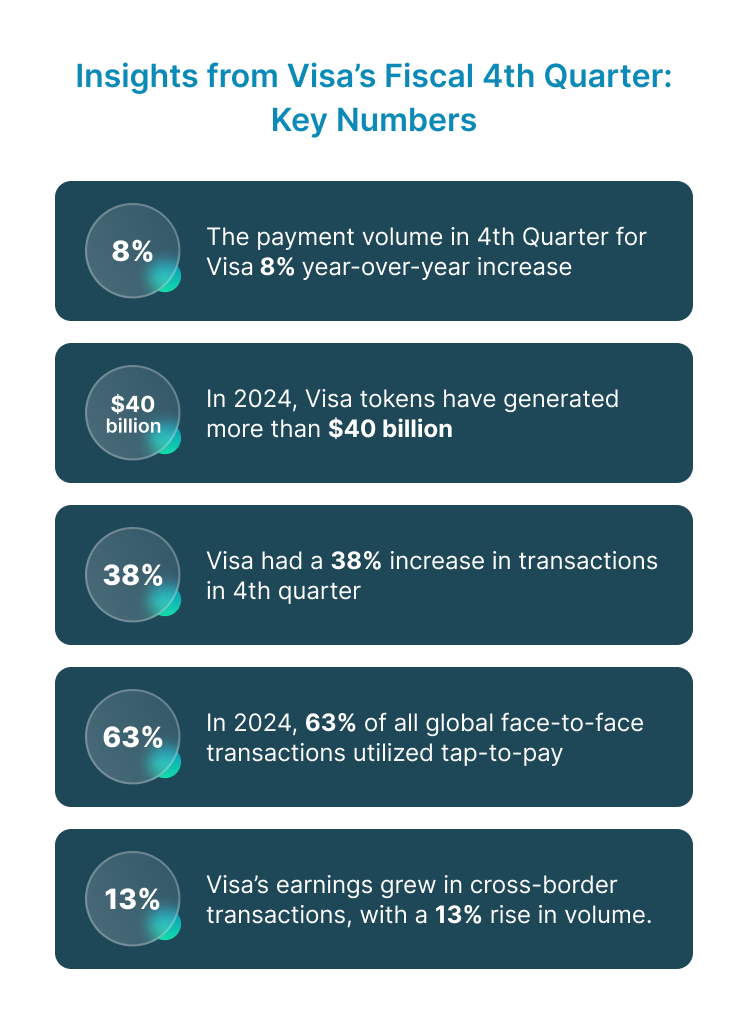

The recent earnings call for Visa's fiscal fourth quarter revealed much more than just strong financial results—it showcased the changing payments landscape and its implications for businesses. With significant growth in Visa Direct transactions and a heightened emphasis on tokenization, Visa is at the forefront of delivering faster, more secure, and seamless payment experiences. The call also emphasized Visa's influence beyond conventional card payments, as new payment flows gained notable traction. Overall, the payment volume experienced an 8% year-over-year increase, highlighting the network's ongoing robustness.

Let’s dive into the key takeaways from Visa’s earnings call and explore how these insights can help payment operations teams prepare for the future.

1. A2A Payments: Simplifying Transactions for a Digital Future

Visa’s push into account-to-account (A2A) payments is a game changer for the industry. Think of A2A as the next step in making payments as simple as moving money from one account to another—direct, secure, and fast. Visa’s CEO, Ryan McInerney, emphasized how Visa’s infrastructure will make these payments more reliable. The upcoming launch in the UK in 2025 hints at a global shift where businesses will need to accommodate digital transactions that bypass traditional card payments.

What does this mean for payment operations?

A2A payments necessitate resilient backend solutions for payment operations teams to manage heightened volumes of non-card transactions. This modification not only streamlines transaction processes but also enables firms to lower interchange fees, hence reducing payment costs. Implementing A2A helps optimize accounting procedures, reduce error rates, and improve security by limiting sensitive data exposure.

Organizations that commence the adaptation of their payment infrastructure to facilitate A2A will be more adequately equipped for a seamless transition to digital-first payment processes as the global market adopts this change.

2. Tokenization: Boosting Security in a World of Digital Payments

Tokenization isn’t just a buzzword—it’s a powerful tool in the fight against fraud. Visa tokens have generated more than $40 billion in incremental e-commerce revenue for businesses globally and saved $650 million in fraud in the last year. By replacing sensitive card data with secure tokens, Visa is making transactions safer for everyone.

Why should this matter to your payment operations?

Tokenization is not merely an optional feature for payment operations; it is crucial for preserving consumer trust and averting financial losses. Tokenization can effectively reduce fraud-related losses and facilitate adherence to rigorous data protection laws, including PCI DSS. Visa research indicates a 26% average decrease in fraud when employing tokens as opposed to conventional online card transactions.

Moreover, research indicates that tokenized transactions have a lower likelihood of decline compared to conventional card transactions, hence facilitating a more seamless checkout experience for consumers. Payment operations utilizing tokenization are likely to see reduced chargebacks, enhanced transaction success rates, and strengthened customer relationships due to increased data security confidence.

3. Visa Direct: Real-Time Payments Are No Longer Optional

Visa Direct continues to take the payments world by storm, with a 38% increase in transactions this quarter alone. In a world where immediacy is everything, real-time payments have become the new standard. With nearly 10 billion Visa Direct transactions by year-end, it’s clear that businesses and consumers alike are demanding faster payment options.

What’s the takeaway for payment operations?

Real-time payments present a substantial operational advantage by improving cash flow management and reducing delays in fund availability. Companies implementing Visa Direct or similar services can offer customers immediate access to funds, thus enhancing loyalty and positioning themselves as competitive players.

In 2021, there were 118.3 billion real-time transactions globally, according to our colleagues at GlobalData, with an anticipated increase to 427.7 billion by 2026, representing 25.6% of all global electronic payments. Research from our partners at the Centre for Economics and Business Research (Cebr), presented here for the first time, demonstrates a distinct association between real-time payments and economic growth. In 2021, real-time payments contributed an extra economic output of $78.4 billion across the 30 nations studied in the Cebr study. By 2026, this amount is projected to increase to $173 billion within the same cohort of nations.

Businesses that adopt real-time capabilities also report higher customer satisfaction rates due to the speed and transparency of transactions. Payment operations teams should therefore focus on upgrading their systems to support instant payments, which can help in reducing transactional friction and meet modern consumer expectations for on-demand services.

4. Tap-to-Pay: The Contactless Revolution Continues

Contactless payments have shifted from being a trend to becoming the standard. Consumers are increasingly embracing tap-to-pay technology for its speed, convenience, and security. In 2024, it was reported that 63% of all global face-to-face transactions utilized tap-to-pay, with this figure rising to 76% for transactions outside the U.S., highlighting widespread international adoption. This shift shows a clear preference for contactless methods in both global and U.S. markets as tap-to-pay becomes the norm in everyday transactions.

What does this mean for your business?

Businesses that neglect to support tap-to-pay options risk alienating a substantial segment of consumers who prioritize rapid and contactless payment methods. Research indicates that businesses adopting contactless solutions experience reduced checkout durations, thereby improving customer satisfaction and operational efficiency.

Enhancing payment systems for tap-to-pay can enable businesses to satisfy consumer demand for convenience while aligning with global payment standards, ultimately delivering a more seamless and competitive customer experience.

5. Cross-Border Payments: The Global Commerce Opportunity

Visa’s earnings call also revealed strong growth in cross-border transactions, with a 13% rise in volume. As global commerce bounces back, businesses are faced with the opportunity—and challenge—of handling more complex international payments.

How should you respond?

Managing cross-border payments demands a safe and flexible infrastructure adept at accommodating various currencies and local rules. The global eCommerce market is projected to exceed $8 trillion by 2027, making it imperative for businesses to seize this opportunity.

Payment operations that emphasize seamless cross-border solutions can lower transaction fees, alleviate risks from currency fluctuations, and access new markets with minimal friction, thus expanding the worldwide client base.

6. Regulatory Pressures: Staying Agile in a Changing Landscape

Visa’s CEO addressed the Department of Justice lawsuit head-on, calling it meritless. This underscores the growing regulatory pressures on payment networks, particularly around competitive practices in the debit card space.

What’s the impact on payment operations?

Payment operations must remain vigilant with evolving regulations. By adopting agile practices and staying current with regulatory trends, teams can avoid penalties, reduce disruptions, and build customer trust. Compliance with standards like GDPR and PCI DSS minimizes risk and aligns with customer expectations, reducing churn through stronger data privacy. Proactively integrating these requirements supports both legal adherence and customer satisfaction, while insights from Visa’s earnings call highlight broader global payment trends such as:

- Increased Digital Transactions: The significant growth in Visa Direct transactions points to a shift towards digital and real-time payments globally. As consumers increasingly prefer seamless digital experiences, businesses must adapt to offer instant payment solutions.

- Cross-Border Commerce Resilience: The 13% growth in cross-border volume suggests that international trade is rebounding, driven by e-commerce and global travel recovery post-pandemic. This trend is crucial for businesses looking to expand their market reach.

- Focus on Value-Added Services: Visa's revenue from value-added services grew by 22%, indicating a strategic shift towards enhancing customer engagement through innovative solutions like marketing services and consulting. This trend reflects a growing demand for integrated payment solutions that provide additional value beyond basic transaction processing.

- Emerging Markets Growth: The significant increase in international payments volume highlights opportunities in emerging markets where digital payment adoption is accelerating. Companies operating in these regions may benefit from tailored solutions that meet local consumer preferences.

Looking Ahead: What Does It All Mean for Payment Operations?

Visa’s earnings call offers a clear vision of where the payment industry is headed—and it’s full of opportunity. From the rise of A2A payments and real-time transfers to the growing importance of tokenization and contactless transactions, the future is digital, fast, and secure.

For payment operations, this means embracing innovation and preparing for a world where payment flows are more diverse and consumer expectations are higher than ever. Businesses that prioritize upgrading their payment systems, integrating security measures such as tokenization, and staying agile in the face of regulatory changes will be better positioned to succeed in this evolving landscape.

Time to Act: Elevate Your Payment Operations Today

The future is here, and Visa’s latest earnings call shows that there’s no time to wait. Whether it’s adopting real-time payments, securing your systems with tokenization, or preparing for the global expansion of A2A payments, the time to act is now. Take a page from Visa’s playbook and ensure your payment operations are ready for the next wave of innovation.

Ready to modernize your payment systems?

Now is the time to assess and upgrade your payment strategies. By embracing the latest trends in payment technology, you can ensure your business stays competitive and secure in a rapidly changing digital world.