Whenever you use your credit or debit card to pay for goods or services, a complicated process happens behind the scenes that includes a number of fees that merchants must pay. Understanding these fees not only helps merchants understand their costs, but it also provides context to the complex yet invisible mechanics facilitating each and every purchase. This blog post will walk you through understanding the three major payment fees including interchange, network, and gateway fees; all written in a plain language, with real data, and from verified sources in order to demystify how much a merchant pays and why.

Interchange fees: The biggest cost slice

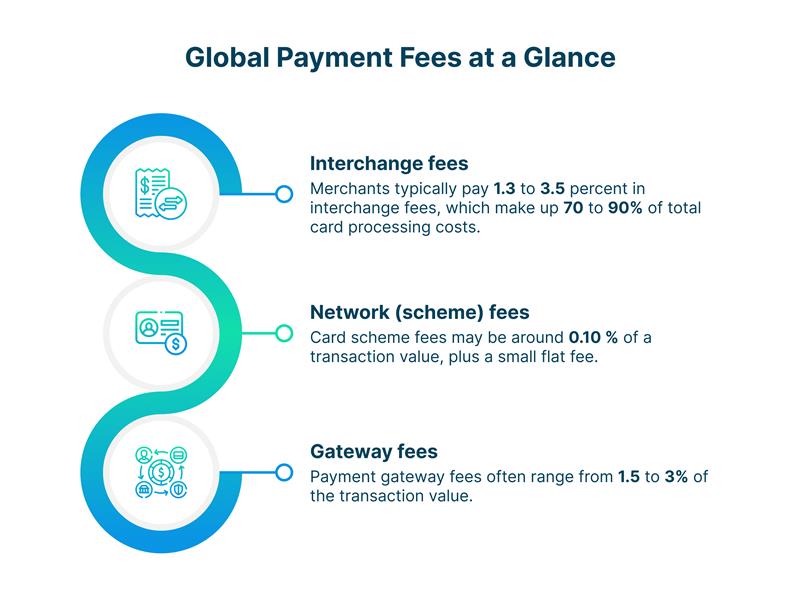

Interchange fees are the largest and most significant part of payment processing costs. They are fees paid from the merchant's bank (called the acquiring bank) to the cardholder’s bank (the issuing bank) whenever a card transaction occurs. These fees compensate the issuer for taking on the risk and costs associated with processing the transaction. Think of the interchange fee as the price charged by the cardholder’s bank for approving your payment and covering fraud protection, credit risk, and rewards programs.

In 2025, interchange fees depend heavily on the card type, transaction method, and merchant industry.

According to Stax, different card networks apply varying interchange fee ranges, and the cost to merchants depends on which card a customer uses. Below is a clear breakdown of those fees:

- Visa: 1.3% to 2.6%

- Mastercard: 1.45% to 2.9%

- American Express: 1.8% to 3.25%

Example: A $100 Visa credit card sale results in $1.30 to $2.60 in interchange fees.

Online sales typically have higher interchange fees than in-person sales due to the increased risk of online selling, typically adding 0.2% to 0.4% to the total contract rates.

These fees update twice yearly (in April and October) to account for changing market dynamics and fraud trends. Debit card transactions usually have lower interchange fees, often below 1.5%, reflecting their lower risk profile.

Special card programs such as corporate, rewards, or prepaid cards influence fee rates by varying degrees, sometimes raising costs. It's worth noting that if transaction data is incomplete or classified as non-qualified, interchange fees can spike, costing merchants over 3% of the transaction.

Network fees: The payment system upkeep charge

Beyond the interchange fees paid to the issuer, card networks like Visa, Mastercard, American Express, and Discover charge what is known as network or assessment fees. Network fees pay for the ongoing maintenance of the global infrastructure to securely and efficiently route payment transactions.

Network fees are generally much smaller than interchange fees, but they are extremely important. Often, the network fees include a percentage (around 0.11%) plus a few cents for each transaction. For instance, if the seller sells a product performing $100, the merchant will likely incur $0.10 to $0.15 in network fees. In summary, network fees play a role in keeping the payments ecosystem thriving, providing for the technology that will enhance the system, fraud protection tools, and fund the operational costs of the system.

Gateway fees: The digital bridge for secure payments

For merchants, particularly those who have online stores, payment gateways are the technology that links your vendor website or point-of-sale system, with banks and card networks. Payment gateways make sure the transactions are securely encrypted, perform fraud checks and process the payment.

Gateway management generally charges fees in three ways: an initial setup fee when you start, a monthly fee while you access the gateway, and a fee per transaction. Transaction fees can range from $0.10 to $0.30 with a small percentage of the overall payment amount processed. While some gateways do not charge a monthly fee, they could take a higher percentage of the transaction instead. The transaction fee covers the technology and operations side of securely exchanging payment information.

Additional fees some merchants face

The chargeback fee that merchants may face typically ranges from $15 to $100, depending on the processor and the specifics of the dispute. For instance, Stripe charges a standard $15 fee for each chargeback filed. Starting June 17, 2025, They introduced a second $15 fee if a merchant contests a dispute and loses it, effectively doubling the chargeback cost in some cases. This second fee is refundable if the merchant wins the dispute. Other processors may charge higher fees, sometimes up to $100, based on their policies and the merchant’s risk profile. These fees cover the administrative and investigative work required to manage the dispute through card networks and banks. Merchants should understand these costs as chargeback fees are generally non-refundable and can add significant expenses, especially if disputes are frequent

Putting It all together: What a merchant pays

To provide perspective on collecting these fees, examine a $100 card payment: