The recent $1.2 billion settlement by Discover Financial Services regarding an overcharge against merchants is a very compelling example of a pitfall of what may be expected to arise in case there isn't enough reconciliation practice. This case demonstrates the need for both transparency and accuracy in payment systems within a business. It also shows the importance of avoiding financial misappropriation to merchants and ensuring fair practices. The most important lesson here is that, even in a world that is ever more dominated by digital payments for commerce, robust reconciliation practices are the key.

The Current State of Payment Systems and Merchant Overcharges

Accenture projects that by 2025, global payments revenues would attain the $2 trillion mark. Such growth brings along complicated fee structures and issues for merchants who rely on payment processors to handle their transactions smoothly. One such pitfall is misclassified fees, as in the case of Discover.

Discover Financial Services agreed to have collected excess fees from merchants for more than ten years because card accounts were misclassified. This means that unnecessary fees inflated merchants' costs substantially. It makes a merchant feel vulnerable since one looks more to the payment processor classifying their accounts than its own way of handling accounts.

The Financial and Reputational Impact of Discover's Misclassification

Discover Financial Services paid a whopping $1.2 billion it owed after overcharging merchants for more than ten years by misclassifying fees. Merchants paid inflated fees to them, at their bottom line, for years without knowing anything about it. It not only affected their book-keeping but their trust in the payment processor was also damaged.

For small and medium-sized businesses (SMEs), even a small increment of the fee greatly impacts the profits. Misclassified merchants in Discover case did not fully manage their overhead, as they neither knew nor controlled extra fees charged to their accounts. Uncertainty over the fee structure left them vulnerable; they could not monitor and appeal such overcharged amounts until it was too late.

The Discover case reminds people of the imperative of transparency in payment processes. Such payment-related errors continue to hurt merchants financially and reputably as the trust of people in payments slowly erodes over time.

Why Effective Reconciliation is Essential for Merchants

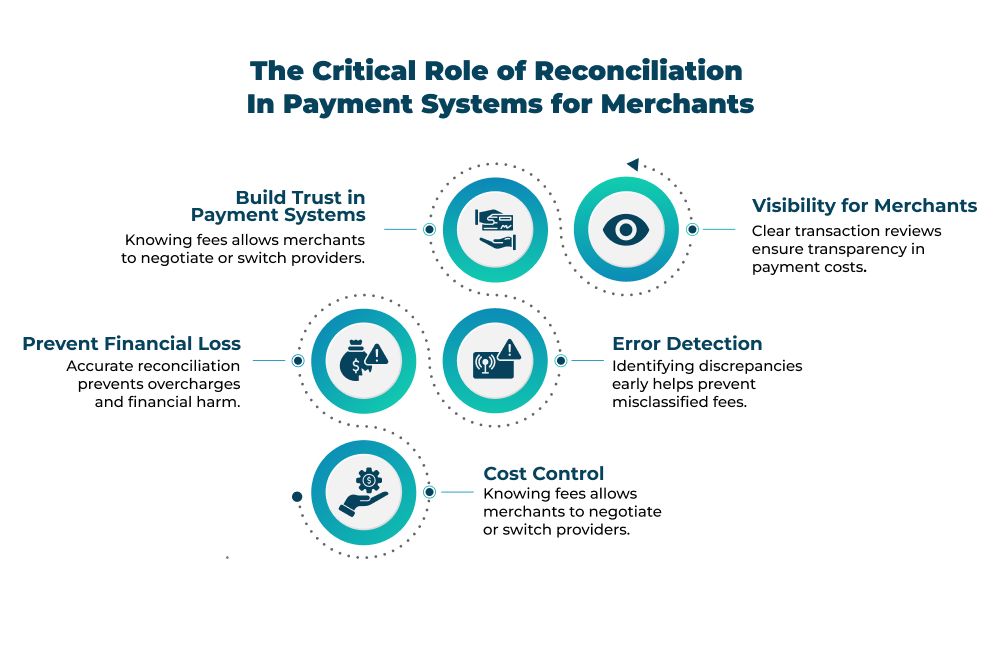

Reconciliation is the process of matching transaction data with corresponding fees to ensure accuracy. This practice is vital for merchants to maintain control over their financial transactions and avoid overcharges. The Discover case shows that without proper reconciliation, merchants tend to bear a risk of being mischarged, sometimes for years, without being able to recognize it.

Here’s how reconciliation can help merchants safeguard their finances:

- Visibility: By meticulously reviewing transactions and associated fees, merchants can have a clear understanding of the costs involved. Notably, 80% of companies fail to verify the credit card charges imposed by payment services and networks. This transparency is crucial for managing finances and ensuring fair practices.

- Error Detection: Reconciliation allows merchants to identify discrepancies in transaction data and fees, helping them catch errors such as misclassification early on. These errors are incurring substantial financial losses for companies. An estimate from the Institute of Finance and Management (IOFM) indicates that 0.2–2% of all global payments are erroneous.

- Cost Control: Understanding the exact fee structure enables merchants to negotiate better rates or switch providers if necessary. In fact, 75% of those verifying credit card charges at a transaction level have decreased their acceptance costs by 18%. This proactive approach to managing costs is essential in a competitive market.

How to Perform an Effective Reconciliation Process to Prevent Overcharges

Reconciliation is more than checking if payments have been received; it has to do with accuracy, reduced risks, and trust in the system by payment processors. A reconciliatory process is important for merchants so they won't be driven into financial errors such as overcharging, misclassified fees, or unnoticed discrepancies.

Steps for an Effective Reconciliation Process:

1. Gather Transaction Data: First, collect all the details of the transactions from your payment processor. This includes charges, fees, and transactions involving multiple accounts.

2. Compare and Match Transactions: Check for consistency in every single transaction by matching it with the corresponding fees and records. In this regard, you are supposed to look out for any inconsistencies double charges, unexpected charges, or failed transactions.

3. Identify Discrepancies Early: Utilize reconciliation tools for identifying errors or discrepancies. Identify them as early as you possibly can before they affect your cash flow or contribute to additional costs.

4. Review Fee Structures: Regularly analyze and question the fees imposed. Understanding fee categories helps you know where to negotiate or switch providers, avoiding costly misclassifications like in the Discover case.

5. Maintain Documentation: Keep clear records of all reconciled transactions for transparency. This documentation is helpful to keep up with audits and also strengthens your ability to resolve disputes with payment processors.

The Discover Incident and the Case for Stricter Regulations

The Discover settlement serves as a wake-up call for the payments industry. It signals a requirement for better regulation or industry norms to make sure the fee models are transparent and well-understood by the merchants. The regulators, like the Consumer Financial Protection Bureau (CFPB), have shown apprehension regarding the impact of big banks merging into each other, such as the currently pending Capital One and Discover deal. When the market is dominated by larger players, then transparency and reconciliations need to be even more accurate.

In order to build trust and maintain integrity in the payments industry, there must be more visibility of and careful watch over how fees are structured as well as communicated to merchants. The payment processors should have standardized practices, so merchants are not blindsided with other hidden or misclassified fees.

How Optimus Fintech Empowers Merchants with Reconciliation Tools

At Optimus Fintech, we understand what goes on in the machinery of payment processing and the critical need for accurate reconciliation. Our technology offers merchants and payment professionals the tools they need to run through complex fee structures across multiple partners with clean efficiency. Our Fees and Commissions module enables:

- Optimize Fee Strategy: Gain insights into the fee structures and leverage this information to optimize costs.

- Enhance Financial Transparency: Have a detailed breakdown of fees and commissions to maintain transparency in payment operations.

- Prevent Overcharges: Ensure accurate matching of transactions and fees, preventing scenarios similar to the Discover incident.

Final Thoughts: Transparency and Vigilance in a Complex Payments Ecosystem

The Discover settlement is far more than a mere financial settlement; it represents an all-important lesson to the payments industry as a whole. It, in fact, showcases the consequences of inadequate reconciliation practices and how important reconciliations are to safeguard the merchants in the payments ecosystem. This aspect - of ensuring transparency and accuracy about fee structures-is going to be critical as the payments ecosystem continues to evolve.

Merchants should be keen about the flow of finances. Payment processors, therefore, have to establish rules and regulations that are in favor of openness as well as fairness. Reconciliation isn't just a wish today; it has become mandatory. In this way, merchants can guard their finances while developing trust for payment partners they choose to cooperate with during uncertain moments in this financial world of intricacy.

It, in fact, showcases the consequences of inadequate reconciliation practices and how important reconciliations are to safeguard the merchants in the payments ecosystem.