Payment Reconciliation

The economics of payment gateways: Where every basis point counts

Why your actual payment processing costs exceed quoted rates. Explore hidden fees, chargebacks, and fraud multipliers eating into merchant margins.

Amrit Mohanty

Jan 20, 2026 (Last Updated: Jan 27, 2026)

Every quarter, when a CFO reconciles their merchant processing statements, the same pattern emerges: the numbers don't match expectations. A transaction marked as 2.6% on the proposal arrives as 3.8% in reality. It happens across industries such as restaurants, e-commerce platforms, SaaS companies, subscription services etc. Merchants assume they understand payment processing economics but most are wrong. The truth is far more complex and far more expensive than any single percentage rate suggests.

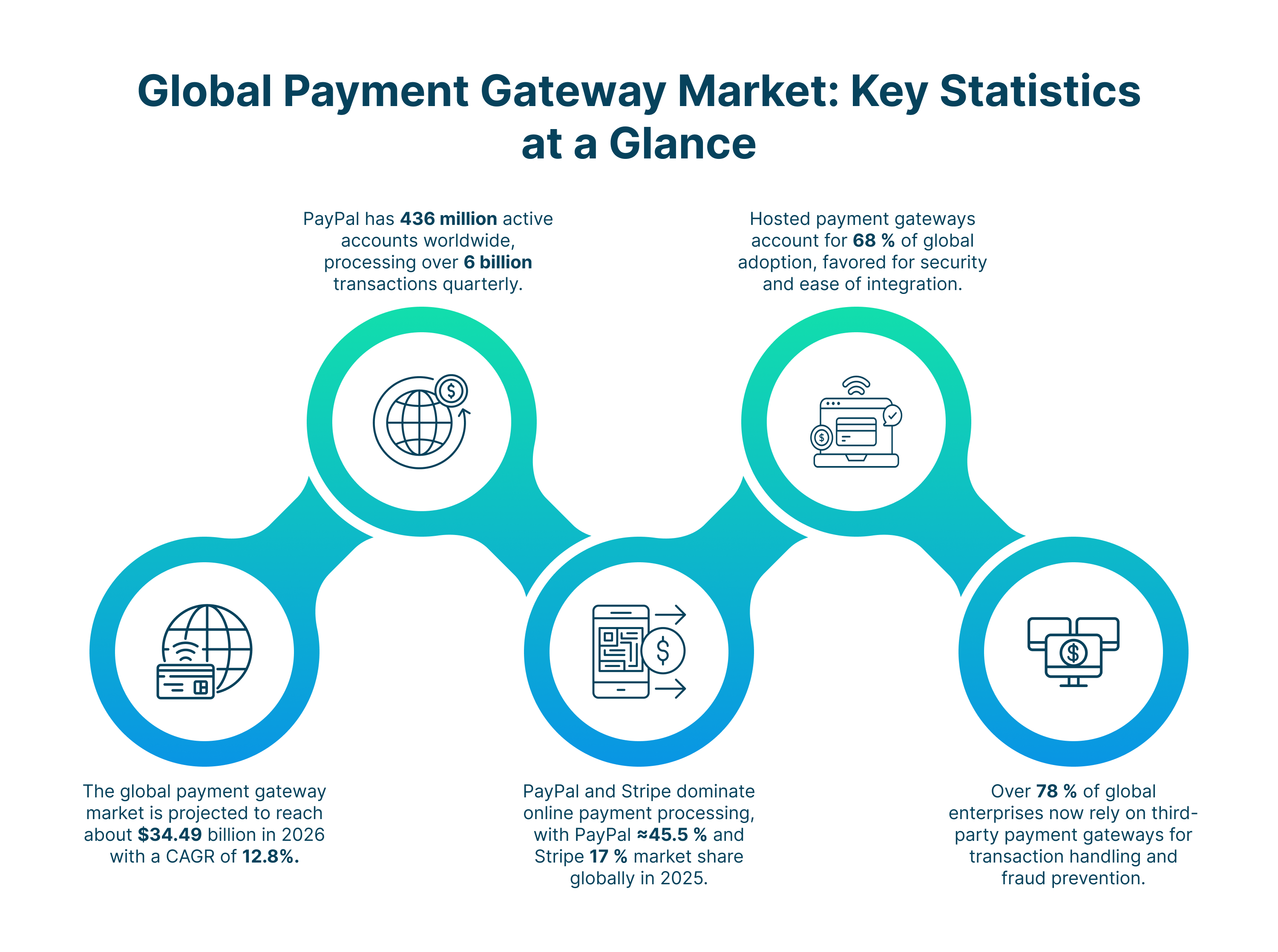

In 2025, Visa processed roughly 260 billion transactions, reinforcing its position as the world’s largest payment network. Mastercard also reported strong momentum, with around 9 % growth in gross dollar volume and a 10 % increase in purchase volume. Yet for many merchants, how that money actually moves through the system remains unclear.

The Rate Deception: What You Quote vs. What You Pay

Payment processors deliberately market their pricing as simple. They quote you a single rate: "2.9% + 30 cents per transaction." It sounds straightforward. It's easy to remember. It's also fundamentally misleading.

That single quoted rate actually conceals three entirely separate cost streams operating independently: interchange (fees that go directly to the card-issuing bank), assessment fees (paid to Visa or Mastercard), and processor markup (the processor's own profit). Each follows different rules, fluctuates on different schedules, and varies based on transaction type. Bundling them into one number makes your costs impossible to understand or negotiate.

Most U.S. merchants now pay between 2.5% and 3.5% in all-in processing costs, yet their contracts specify rates at the lower end of that range. The gap isn't an error; it's the intended architecture of payment processing economics.

The Three Layers Affecting Your Margins

Layer One: Interchange; The Non-Negotiable Baseline

Visa interchange ranges from 1.15% + $0.05 to 2.40% + $0.10 per transaction, while Mastercard's rates span 1.45% + $0.05 to 2.90% + $0.10. These rates are published twice yearly by the networks themselves. Your processor cannot reduce them. You cannot negotiate with them. They are fixed costs disguised as percentages.

The key insight: interchange varies dramatically by card type. A business-class Amex transaction costs three times more than a standard debit card. Your most profitable customers often use your most expensive payment method.

Layer Two: Network Assessments and Processor Markup

After interchange, companies such as Square, Stripe, and PayPal layer their markup on top, typically 0.20% to 1.0%. This is where your processor extracts profit. They route transactions, assume risk, manage disputes, and maintain infrastructure. That markup is their business model.

The problem: processors bundle everything into a single percentage, obscuring whether you're paying 0.30% or 0.75% in true processor costs.

Layer Three: Transaction-Specific Penalties

Card-not-present transactions carry premiums because fraud rates are higher and chargebacks more frequent. Online merchants pay more than in-store merchants for the identical card used by the identical cardholder. Subscription payments carry different rates than one-time purchases. Business cards cost more than consumer cards.

The Fraud and Chargeback Multiplier Effect

Here's where payment processing economics becomes genuinely punishing.

For every dollar lost to fraud, U.S. merchants now pay $4.61 in total losses, representing a 37% increase since 2020. A $20 transaction fraudulently disputed doesn't cost you $20. It costs you $20, the chargeback fee ($15–$100), the lost product cost, shipping, processing labor, and potential account penalties.

The volume problem is accelerating. Global chargeback volume is projected to reach 324 million transactions by 2028, up from 261 million in 2025. Chargebacks will cost merchants $41.69 billion by 2028.

But the cruelest fact: between 61% and 80% of chargebacks involve valid transactions where customers dispute charges they authorized. This isn't fraud prevention, this is pure profit transfer.

Card-not-present transactions experience chargeback rates between 0.6% and 1.0%, significantly higher than the 0.5% rate for in-person transactions. An online merchant processing $500,000 monthly absorbs $3,000 to $5,000 in chargebacks before calculating any fees.

The Regulatory Ratchet: Compliance Costs Rise While Negotiating Power Falls

Visa's Acquirer Monitoring Program (VAMP) creates escalating penalties: merchants with chargeback rates exceeding 0.9% face $10 fees per disputed transaction plus elevated processing fees starting January 1, 2026. This regulatory pressure doesn't reduce fraud; it shifts costs onto merchants already struggling with chargeback volume.

The perverse incentive: merchants reduce fraud prevention spending to cut costs, which increases chargebacks, which triggers higher fees, which further compresses margins.

Building an Economy Beyond Credit Cards

Not all payment methods cost the same. Merchants who ignore this leave thousands annually on the table.

ACH payments (bank transfers) typically cost $0.20 to $1.50 per transaction, far less than percentage-based card pricing. A $10,000 transaction costs $10 to $150 via ACH versus $250–$350 via credit card. Bank transfers also enjoy dramatically lower fraud and chargeback rates.

Regulated debit in the U.S. costs approximately $0.21 plus 0.05% of the sale, typically yielding an effective cost under 1%, a dramatic improvement over premium credit cards.

The barrier isn't economics; it's adoption. Over 85% of merchants now plan to accept alternative payment methods within the next one to three years, but most still default to credit card-first checkout flows.

The Optimization Framework

Merchants winning in 2025 treat payment economics as a competitive advantage, not an afterthought.

First: calculate your true effective rate. Total fees divided by total volume. If it exceeds 3%, demand an explanation.

Second: diversify payment methods intentionally. Offer ACH prominently. Educate customers on debit options. Reward alternative payments with faster processing or discounts.

Third: implement fraud controls strategically. A $500 monthly detection service prevents far more loss than it costs.

Fourth: negotiate from data. If you process hundreds of thousands annually, demand interchange-plus pricing. Everything except basic interchange is on the table.

The Bottom Line

Your payment processing cost isn't a single percentage, it's a dynamic ecosystem where every participant extracts value. Interchange gets blamed because it's visible and regulated. But your processor, card networks, fraud systems, and chargebacks quietly consume far more of your revenue.

One basis point; one hundredth of a percent represents real margin on thousands of monthly transactions. The merchants thriving today are those who refuse to accept quoted rates at face value, who calculate effective costs obsessively, and who systematically shift transaction volume toward cheaper payment methods.

You can reach us at:

1700 Montgomery St, San Francisco, California 94111

6470 E Johns Crossing Suite 160, Johns Creek, GA 30097

Copyright © 2026 Optimus. All Rights Reserved.