A card payment clears in seconds. Smooth. Done. But here's what you don't see: behind that seamless transaction are dozens of data fields such as interchange category, authorization codes, routing paths, settlement references, fee components and more.

And all of it has to be right!

Here's the problem. When even one of those attributes is wrong, the payment still goes through. Your customer doesn't notice. You don't notice. Not immediately anyway. But that cost? It doesn't show up on the receipt. It shows up weeks later when you are reconciling accounts, noticing revenue leakage, fielding customer disputes, and dealing with audit flags.

For CFOs, fintech leaders, and enterprise operations executives, this is why payment data accuracy has become so critical. It's not just a technical thing anymore. It's what determines whether your business can actually predict its finances, scale without breaking things, and maintain the trust you have built.

Why Payment Data Accuracy Has Become a Strategic Issue

Data quality in payments spans far more than settlement. It underpins forecasting, reconciliation, compliance reporting, fraud detection, and customer experience. When inaccuracies enter the transaction lifecycle, they propagate across ERPs, payment gateways, bank feeds, and analytics systems, triggering revenue recognition delays, ballooning exception volumes, creating settlement mismatches, and stacking audit exposure. One wrong field breaks multiple systems at once.

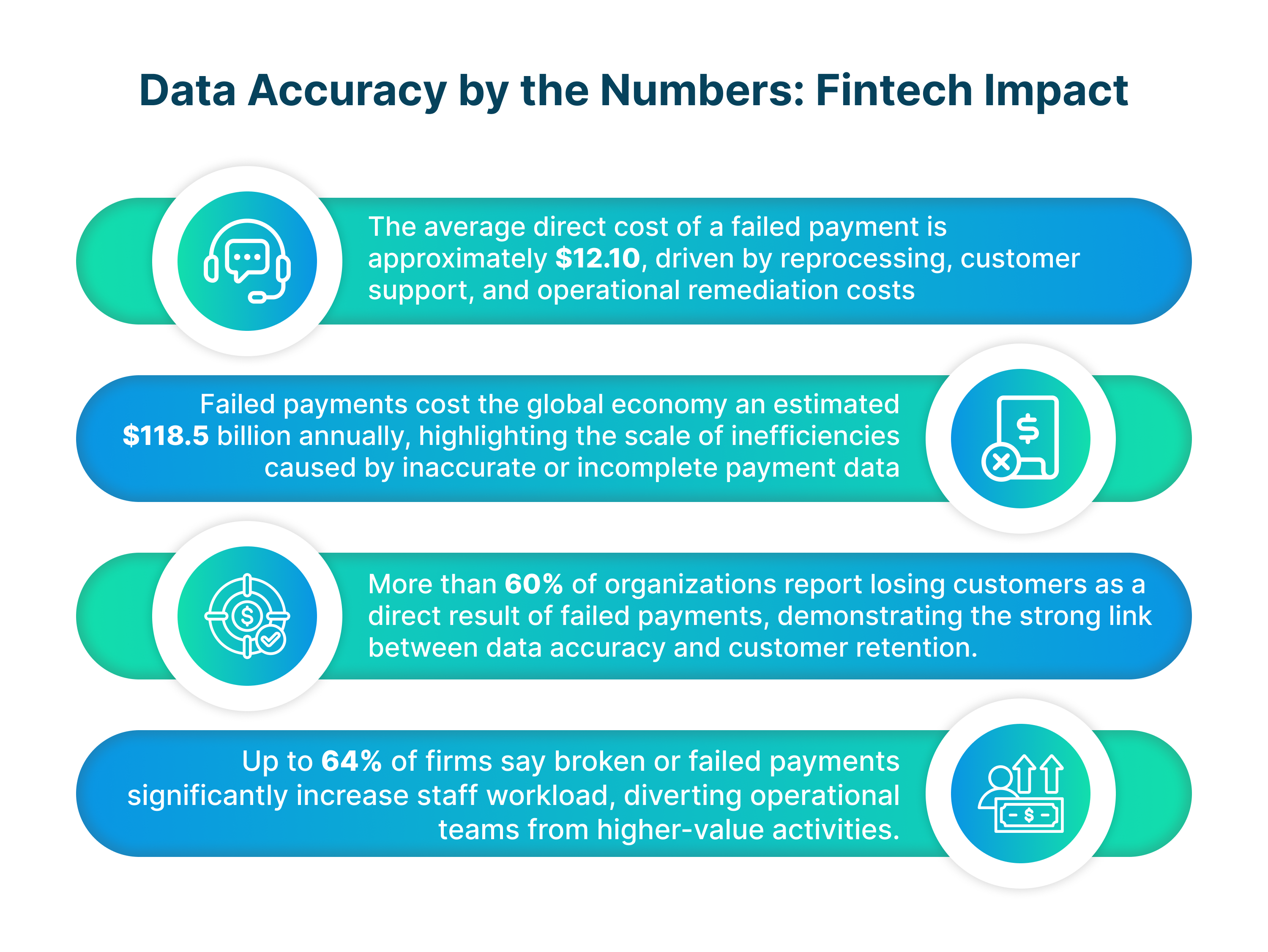

The economic consequences are substantial and well-documented. IBM estimates that bad data costs U.S. businesses $3.1 trillion annually, a figure encompassing lost productivity, rework, and missed opportunities. Within financial services, the impact is more acute. Gartner's research found that organizations lose an average of $15 million per year to data quality failures.

For payment operations, these numbers understate the true risk. Error rates that appear marginal at the transaction level become material at scale. Multiply a 0.1% error rate across millions of daily transactions, and you are looking at systematic leakage that compounds across reconciliation, compliance, and revenue recognition cycles.

CFOs: When Payment Data Distorts Cash Flow and Margins

For CFOs, payment data accuracy directly affects cash visibility and financial control. Incorrect transaction data distorts working capital metrics, triggers revenue recognition delays, and creates settlement mismatches between invoices and bank records. Finance departments are forced into reactive reconciliation cycles, managing swelling exception volumes weeks after problems originate. The result: audit exposure compounds, and the window to resolve issues closes.

This challenge is increasingly recognized at the executive level. A PYMNTS survey found that 90% of CFOs want greater automation to reduce payment errors and delays, citing the negative impact on cash flow predictability and operational efficiency. The issue is not simply speed, but trust: forecasts are only as reliable as the transaction data feeding them.

Manual reconciliation remains one of the most expensive hidden costs. Each exception requires human intervention, lengthening close cycles and quietly eroding margins. Over time, these small inefficiencies accumulate into systemic financial drag.

Fintech Leaders: Scaling Amplifies Data Accuracy Risk

As Fintechs are designed for rapid growth, they can handle numerous transactions through several different platforms. For Fintech companies, ensuring the accuracy of data is not just a secondary concern. Rather, data accuracy is essential for rapidly scaling the company. If a customer makes a payment incorrectly, routes it incorrectly, or somehow otherwise mishandles the payment process, it creates additional "friction" in their experience with the company, leading to increased operating costs and an escalation in customer dissatisfaction.

According to research within the payment industry, the average cost of a failed payment (including reprocessing, network fees, and customer service support) is approximately $12 for each transaction. While this figure may seem relatively low per transaction in isolation, when the total number of failed payments is multiplied by the number of transactions that occur annually, the costs become more significant.

The inaccuracies in payment data also have a significant impact on engineering and operations because they take time away from the development of innovative products to address mismatches and exceptions. This creates a strategic trade-off for fintech company leaders. As such, the growth of their enterprise will be hindered by a lack of data accuracy and therefore slow down.

Enterprise Operations: Where Data Issues Become Customer Problems

Enterprise operations teams experience the impact of poor payment data most immediately. Inaccurate or incomplete transaction records are a primary driver of customer service inquiries, disputes, and escalations. Each payment exception increases handling time, inflates support costs, and introduces friction into the customer journey.

Research from LexisNexis Risk highlights how transaction failures and data inconsistencies increase operational risk and customer dissatisfaction in digital payments environments. More importantly, customer behavior following payment failures is unforgiving. Studies show that a meaningful portion of customers do not retry failed payments, and repeated issues significantly reduce customer lifetime value.

At an enterprise level, payment accuracy is inseparable from brand trust. While customers are generally willing to accept a delayed shipment or slow responses, when a payment fails, there is a significant loss of trust and confidence from the customer’s perspective.

Regulatory and Compliance Implications

As regulators closely monitor Payment Data Accuracy, Financial Institutions and Payment Providers must maintain full, consistent and auditable records of transactions. If data is not accurate, it may result in inaccurate reporting, audit failures and regulatory fines for jurisdictions that have very strict and comprehensive consumer protection and Financial Transparency laws.

Academic and industry research links poor data quality to increased compliance risk, especially in regulated payment and banking environments. What begins as an operational issue can quickly evolve into a legal and reputational one.

Reducing the Hidden Cost of Transactions

Leading organizations are addressing payment data accuracy by shifting prevention upstream. Straight-through processing minimizes manual touches and stops the spread of errors to various systems across the enterprise. Real-time validation guarantees that payment data is accurate when created, and not post-settlement. More businesses use AI tools to find anomalies, errors and breaks in reconciliation on a large scale.

Most importantly, high-performing businesses view payment data as a managed asset. They clearly define who owns payment data, have defined data standardization and hold all functions responsible for ensuring the accuracy of payment data.

Conclusion

The visible cost of a payment is rarely its true cost. Beneath every transaction lie hidden expenses such as manual effort, customer friction, lost trust, and regulatory exposure, all driven by inaccurate data. For CFOs, fintech leaders, and enterprise operations executives, improving payment data accuracy is not about incremental optimization. It is about protecting margins, enabling scale, and sustaining trust.

This requires a fundamental shift. Payment data must be treated as a managed financial asset, not a byproduct of settlement. It demands transaction-level reconciliation that catches errors before they propagate, fee and commission validation that prevents leakage, and real-time anomaly detection that surfaces problems as they emerge.

In a digital economy where payments are instant and expectations are unforgiving, data accuracy determines whether transactions create value or quietly destroy it.