With every credit card swipe, merchants, whether they're restaurants, stores, delis, or online giants such as Ebay or Amazon, incur fees to credit card companies, processors, and banks. Online transactions carry even higher fees due to the increased risk of fraud. As more people shift to online shopping and utilize their cards for various reasons like convenience or reward points, these fees become more prevalent.

Selecting a payment processing service can feel daunting due to the multitude of credit card processing fees involved. It's vital to find a provider that accepts various forms of payment (Visa, Mastercard, Discover, American Express, PayPal, etc.) while prioritizing the security of your customers' information. In 2022, U.S. credit card companies earned $126.4 billion from merchant processing fees. Reports further indicate Visa and Mastercard plan to raise fees further in 2023 and early 2024.

Navigating the intricate realm of credit card transactions is crucial for maintaining profitability and sustainability, whether you're a finance expert or a small business owner. In this blog, we'll explore the complexities of credit card fees and offer practical strategies for managing them effectively.

Decoding the Fee Structure

Did you know that the average credit card processing fee ranges between 1.5% and 3.5%? Credit card fees are often determined by a number of variables, such as required and negotiable costs incurred by the card issuer, payment processor, and card network. They can be complex because they cover a wide range of factors that affect your profit margin. Let's dive deeper into the key players in this complex ecosystem:

Interchange Fees

- Interchange fees are essentially the tolls paid for using the credit card network. They're charged by the card-issuing bank to the merchant's bank for processing each transaction.

- These fees are non-negotiable and typically make up the largest portion of credit card fees. They vary based on factors such as the type of card used, the transaction method (e.g., in-person vs. online), and the merchant's industry.

- The bank issuing the credit card receives the interchange fee. For instance, if you hold a Visa credit card from Chase, Chase receives the interchange fees for your transactions.

Assessment Fees

- Assessment fees are charged by card networks such as Visa and Mastercard and contribute to network maintenance and development.

- Similar to interchange fees, assessment fees are calculated as a percentage of the transaction volume. The average cost of assessment fees typically ranges between 0.13% to 0.15%.

- They help fund the infrastructure and services provided by the card networks, including fraud prevention measures and technological advancements.

- While merchants can't negotiate assessment fees directly with the card networks, understanding their role in the overall fee structure is essential for managing costs effectively.

Merchant Service Charges (MSC):

- MSC, imposed by the merchant service provider (MSP), encompasses a variety of fees for processing credit card transactions. For credit cards on an average it is between 0.3% to 0.9%.

- These charges can include flat fees, percentage fees based on transaction volume, and incidental fees for specific services or circumstances.

- Merchant service charges cover the costs associated with providing payment processing services, including equipment, customer support, and compliance with industry regulations.

Incidental Fees

- In addition to interchange, assessment, and merchant service charges, merchants may incur incidental fees for specific events or circumstances.

- Examples of incidental fees include chargeback fees (for disputed transactions), retrieval request fees (for providing transaction documentation), and non-compliance penalties (for failing to meet regulatory requirements).

- While incidental fees may be less common, they can still impact your overall expenses and should be monitored closely to avoid unexpected costs.

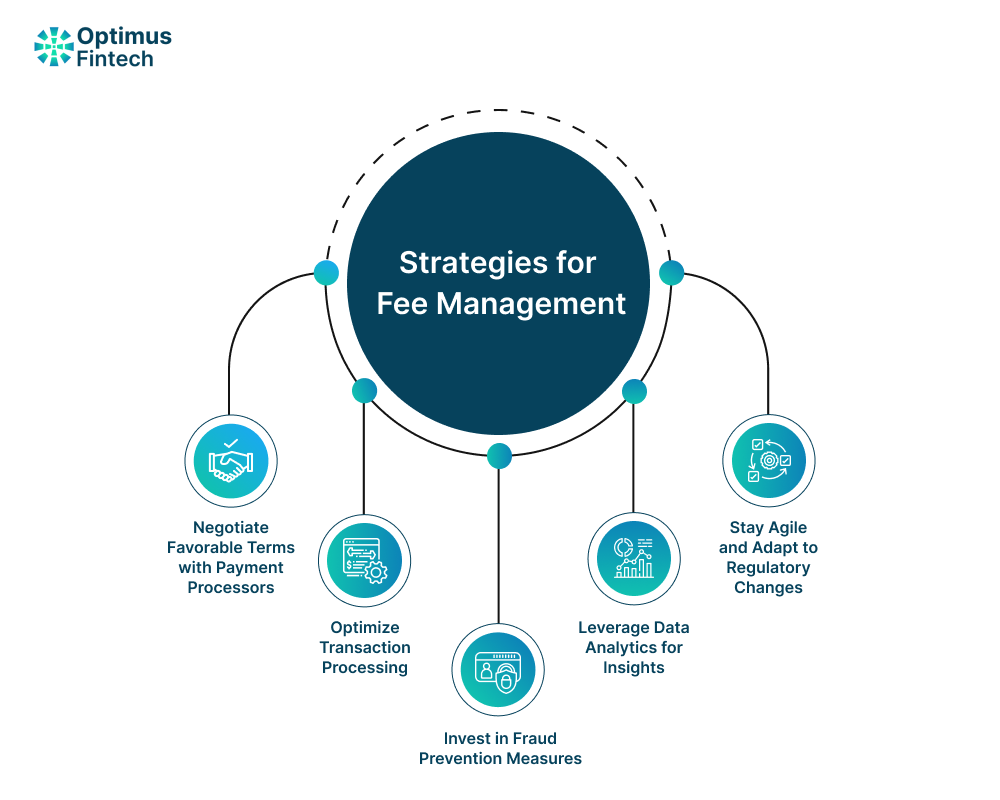

Strategies for Fee Management: Meeting the Challenges of Credit Card Transaction Costs

Navigating the complexities of fee management in credit card transactions is vital for sustaining profitability and competitiveness. Challenges such as rising interchange fees and regulatory compliance costs demand strategic solutions. Here, we highlight key challenges and effective strategies for managing fees efficiently:

1. Negotiate Favorable Terms with Payment Processors:

- Challenge: Rising interchange fees set by card networks pose a significant challenge for businesses. Negotiating with payment processors for favorable terms can help offset these increasing costs.

- Strategy: Engage in proactive negotiations with payment processors to secure lower interchange rates based on factors such as transaction volume, card types, and industry risk. Leverage competitive offers from multiple processors to negotiate better terms.

2. Optimize Transaction Processing:

- Challenge: Inefficient transaction processing methods can lead to higher merchant service fees and operational inefficiencies.

- Strategy: Implement technology solutions and transaction processing optimizations to streamline operations and reduce costs. Utilize advanced payment gateways, point-of-sale systems, and automated reconciliation tools to enhance efficiency and minimize processing expenses.

3. Invest in Fraud Prevention Measures:

- Challenge: Fraudulent transactions and chargebacks result in financial losses and increased processing costs for businesses.

- Strategy: Invest in robust fraud detection and prevention measures to mitigate risks and protect against unauthorized transactions. Implement multi-layered security protocols, including tokenization, encryption, and real-time transaction monitoring, to identify and prevent fraudulent activity.

4. Leverage Data Analytics for Insights:

- Challenge: Limited visibility into transaction data and trends hinders effective fee management and decision-making.

- Strategy: Harness the power of data analytics to gain insights into transaction patterns, customer behavior, and fee structures. Analyze transaction data to identify cost-saving opportunities, optimize pricing strategies, and forecast future fee trends.

5. Stay Agile and Adapt to Regulatory Changes:

- Challenge: Compliance with evolving regulatory standards, such as PCI DSS and government regulations, imposes additional costs and complexities on businesses.

- Strategy: Stay informed about regulatory changes and proactively adapt compliance measures to ensure adherence to industry standards. Invest in staff training, conduct regular audits, and implement robust security protocols to minimize the risk of non-compliance and associated penalties.

The Road Ahead

In an increasingly cashless society, credit card transactions are here to stay. By understanding the intricacies of transaction fees and implementing proactive management strategies, businesses can navigate this landscape with confidence and profitability.

Remember, fee management is not a one-time task but an ongoing effort that requires vigilance, adaptability, and a keen eye for optimization. Stay informed, stay proactive, and reap the rewards of effective credit card fee management at scale.