Payment Reconciliation

Why Modern Payment Systems Need Governance, Not Just Automation

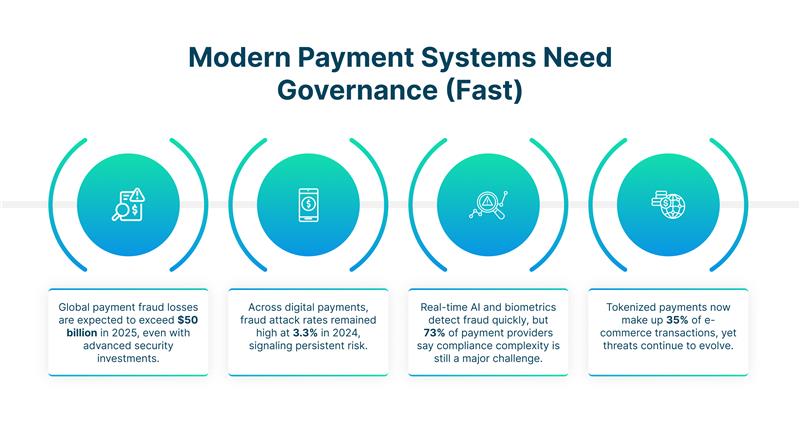

Modern payment systems need more than automation; governance ensures security, compliance, fraud control, and long-term scalability.

Amrit Mohanty

Feb 17, 2026 (Last Updated: Feb 25, 2026)

You have heard this many times; "automation is the future".

According to the McKinsey Global Payments Report 2025, $2.5 trillion of revenue, 3.6 trillion transactions occur every year through banks because of the use of AI and the transactions are quicker than ever through "real-time" processing while at the same time the level of innovation is at light speed compared to that of governing bodies trying to keep up with the pace of the automation movement.

The Uncomfortable Truth

When a bank deploys AI fraud detection, costs plummet. Processing times shrink and executives celebrate.

What's missing from that celebration? You have moved the risk, not eliminated it.

LSEG Risk Intelligence tells us clearly: AI doesn't replace fraud practices. It enhances them. Criminals adapt. They probe your models. They find edges. New threats emerge; model drift, adversarial attacks, silent failures nobody's watching.

Here's what really stings: according to compliance research, only 18% of AML professionals have fully operational AI tools. Yet 71% of organizations are using AI in financial operations. That gap is where systemic risk lives.

Just imagine, a customer gets flagged by an algorithm. Their account freezes instantly. No explanation, no appeal, no human checks. They are locked out of their own money. This isn't theoretical, this is happening right now.

The Regulatory Reckoning

The U.S. SEC initiated 200 enforcement actions in Q1 2025 alone. That pace hasn't happened since 2000. Two hundred cases in three months! Global regulators issued $2.3 billion in AML fines in that same quarter. Billions. Not millions. Billions in one quarter alone.

Central banks in India and Canada mandate real-time monitoring now. They are tightening oversight because they want transparency. They are saying: "We need to see inside the black box." However, here is the critical problem: only 28% of organizations have formal AI policies. Yet 71% are using AI in their financial operations.

Do you see that gap? Two out of three compliance teams are trying to govern AI systems they don't have tools to understand. They are flying blind, hoping it works. Also knowing they will take the fall if it doesn't.

The Hybrid Model Works

89% of compliance professionals say AI speeds their work. True. AI is useful.

But 91% of organizations maintain centralized governance teams. Nine out of ten. They are doubling down on human oversight.

The Payments Association pushes beyond identity data. Monitor behavior. Track devices, watch patterns, this requires judgment. A machine flags a transaction. A human understands why. The machine accelerates. The human brings wisdom. That partnership works.

Regulatory Framework Tightens

The GENIUS Act (July 2025) introduced major changes to stablecoins, requiring 100% reserves and mandating strict reporting standards. ISO 20022 adoption by Fedwire (July 2025) improved structured data handling significantly. Swift ends coexistence by November 2025.

These are regulatory signals from the top: ‘Transparency is now mandatory.’

Manual review drops. But it's being replaced with transparent systems. Fraud detection happens faster and reasoning gets documented. Every decision has a paper trail and regulators demand operational resilience.

Sanctions screening in seconds. Fraud detection within days. Speed and accuracy aren't the only metrics. Explainability, auditability, resilience matter now.

What Governance Actually Means

Real-time audit trails maintain institutional memory. Document every decision. When AI makes thousands of choices per second, you need to know what happened and why.

Explainability requirements are non-negotiable. Why flagged this? Why reject that? Black boxes fail compliance. Customers deserve to understand why their money was frozen.

Human escalation paths matter. AI detection happens in milliseconds. But friction, intentional slowdown matters. Legitimate customers deserve human judgment at critical moments. That human touch? That's real trust and dignity.

Third-party oversight isn't bureaucracy. Your vendors carry concentration risk. If they fail, you fail. Clear contracts matter.

The Bottom Line

Winners in 2025 won’t be the fastest; they will be the smartest, automating intelligently with governance built in from day one, not bolted on later.

Companies racing ahead without governance frameworks are playing dangerous games. They think speed is an advantage. They think automation is a victory, but is it really?

The SEC's 200 enforcement actions and $2.3 billion in fines aren't accidents, they are warnings. Speed without governance isn't innovation. It's recklessness. It freezes customers' accounts without explanation. It crashes systems when vendors fail. It costs billions in fines and destroys reputation.

The future of payments isn't about who moves fastest. It's about who moves fastest responsibly. Who embeds human judgment into automated systems. Who makes explainability a feature. Who builds governance as infrastructure.

McKinsey, Deloitte, and the Federal Reserve all agree: governance and automation are partners, not competitors.

So here's the real question: Will you govern as you go? Not after you scale. Not when regulators force you. Now. While you can build it right.

The payments system processes 3.6 trillion transactions yearly. That scale demands both speed and responsibility. Both automation and judgment. Both innovation and trust.

Winners won't be the fastest. They'll be the ones who understood that in a system built on belief, speed without accountability destroys everything.

That's the real partnership that matters. That's survival.

You can reach us at:

1700 Montgomery St, San Francisco, California 94111

6470 E Johns Crossing Suite 160, Johns Creek, GA 30097

Copyright © 2026 Optimus. All Rights Reserved.