Payment costs rarely announce themselves as a problem. They sit quietly inside processor statements, spread across geographies, and bundled under labels that rarely invite scrutiny. Yet in aggregate, they have become one of the most persistent margin drains for modern enterprises.

In the United States, merchants paid an estimated $187.2 billion in card processing fees in 2024, driven not only by transaction growth but also by layered network fees, processor markups, and ancillary charges that are often poorly disclosed

For CFOs managing businesses with operating margins in the single digits, even small inefficiencies in payment economics can erase a meaningful share of net profit, often without triggering internal alarms.

Complexity Is Accelerating

Payment cost complexity is increasing faster than most finance teams can track manually. In the US, card networks have introduced dozens of new or modified fees over the past decade, many tied to security programs, data usage, or network infrastructure rather than transaction value. According to the Nilson Report, total US card fees have grown faster than card purchase volume, indicating rising cost density rather than pure scale effects.

In Europe, despite interchange fee caps, non-interchange scheme fees continue to expand. This growing complexity makes static reviews insufficient and reinforces the need for continuous visibility rather than periodic audits.

When Forecasts Lose Precision

Opacity in payment costs doesn’t just affect margins. It undermines financial predictability.

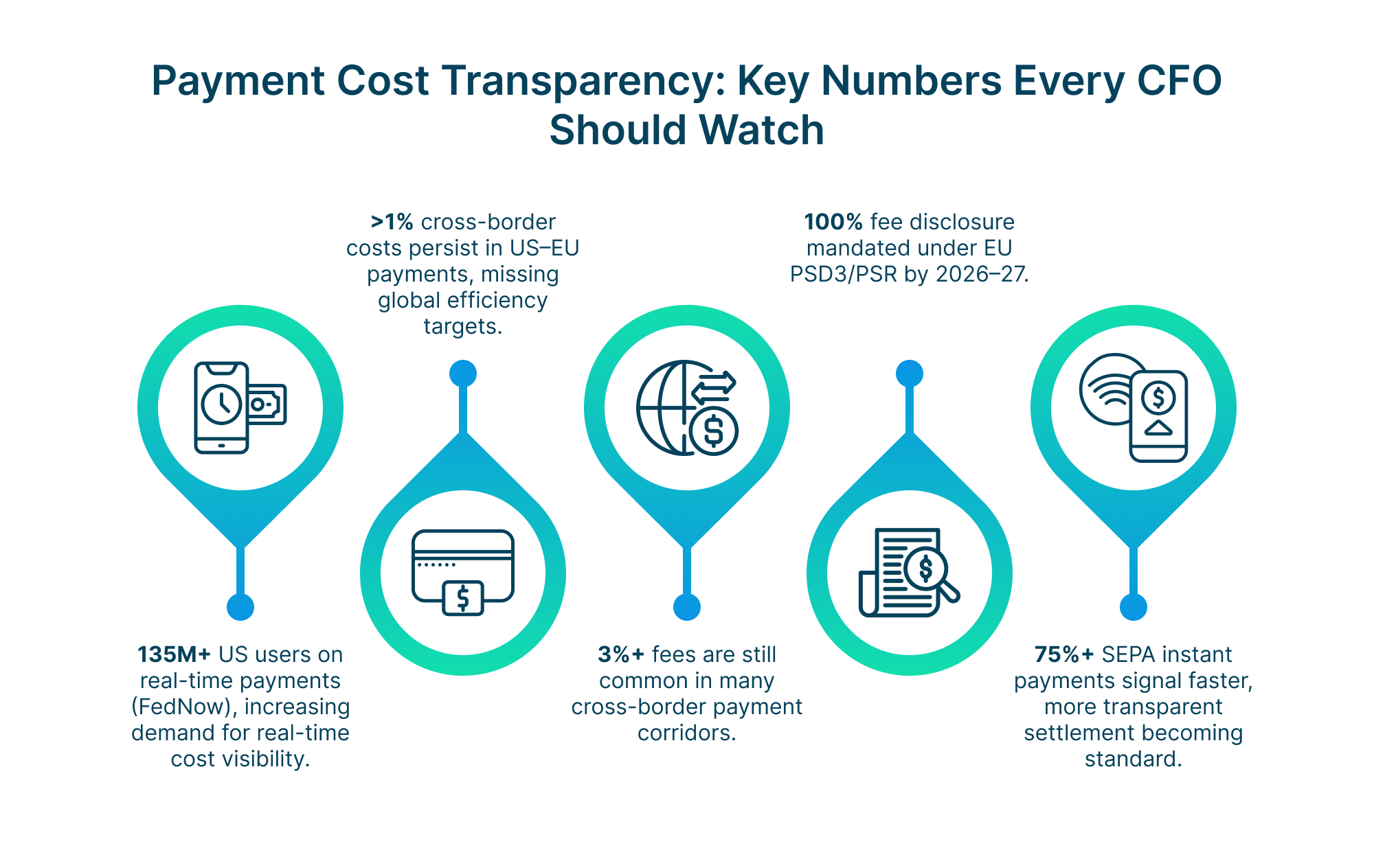

Settlement timing, variable interchange rates, cross-border premiums, and FX spreads introduce volatility that rarely appears in revenue models. In the US and Europe, cross-border card transactions commonly incur additional fees ranging from 0.6% to 2%, depending on card network and region

Without clear visibility into these variables, finance teams are forced to pad forecasts and over-allocate working capital. This leads to lower confidence in cash flow projections, an increasingly uncomfortable position in capital-constrained environments.

Data Is Negotiation Currency

Payment providers negotiate from a position of informational advantage. When fee structures are bundled and reporting lacks granularity, enterprises struggle to benchmark pricing or challenge increases effectively.

This imbalance has drawn regulatory attention in Europe. The UK Payment Systems Regulator found that Visa and Mastercard increased scheme and processing fees by around 25% above inflation between 2017 and 2023, costing UK businesses an estimated £170 million annually.

For CFOs, the message is clear. Negotiation leverage is built on data, not transaction volume alone.

Margin Pressure Meets Investor Expectations

Investor scrutiny around unit economics is intensifying, particularly in capital-constrained markets. In the US, public companies are increasingly challenged on gross margin sustainability, where payment costs directly reduce reported margins. Research from McKinsey indicates that payment-related costs can account for up to 20–30% of total revenue leakage in certain digital and subscription-heavy business models.

In Europe, where growth expectations are more conservative, investors place even greater emphasis on cost discipline. CFOs who can clearly explain and optimize payment economics are better positioned to defend margins and maintain market credibility.

The Cost of Inaction

When payment costs remain opaque, the financial impact compounds quietly. Fee increases go unnoticed, contract renewals default to existing terms, and inefficiencies gradually become embedded in the cost structure.

Across the US and Europe, card networks and processors regularly introduce new fees or reclassify existing ones. Without continuous visibility, these changes are absorbed rather than challenged. Over time, finance teams lose control over one of the most scalable cost lines in the organization, often realizing the impact only after margins have materially shifted.

From Compliance to Scrutiny

Regulators are no longer treating payment fees as a purely commercial concern.

In Europe, policymakers continue to push for greater disclosure and pricing transparency, citing the cumulative burden of opaque fees on businesses despite interchange caps.

In the US, ongoing scrutiny of card network pricing practices is raising expectations that enterprises can clearly explain and justify payment costs.

Payments as a Strategic Lens

The most forward-looking finance leaders are reframing payments from infrastructure to insight.

With granular visibility, CFOs can identify which payment methods suppress margin, which regions carry disproportionate friction, and where customer experience trade-offs conflict with profitability. This insight supports smarter decisions on pricing, market entry, fraud tolerance, and cost-to-serve.

A Signal of Financial Maturity

Payment cost transparency has also become a marker of financial maturity.

Organizations that can clearly articulate their payment economics to boards, investors, and auditors signal strong governance and disciplined financial management. As capital markets place greater emphasis on unit economics and cash efficiency, CFOs are expected to demonstrate not just revenue growth, but the quality and durability of that revenue.

The CFO Imperative

In an environment defined by margin pressure, regulatory momentum, and investor scrutiny, payment cost transparency is no longer optional.

For modern CFOs, the question is no longer whether payment costs matter. It is whether the organization truly understands them. What remains opaque cannot be optimized, forecasted, or defended.