Impact on Financial Operations

The integration of Afterpay into Cash App is expected to have several implications for financial operations:

- Increased User Engagement: The addition of BNPL services may drive higher transaction volumes within the Cash App ecosystem. Block reported that its BNPL services generated a gross merchandise value of $8.24 billion, reflecting a 23% increase year-over-year.

- Revenue Growth: Afterpay has become a significant revenue stream for Block, contributing approximately $242 million in gross profit from BNPL services in the last quarter alone. This indicates a robust demand for flexible payment options that could further enhance Block's overall profitability.

- Financial Inclusion: The partnership aims to address the needs of underbanked populations by providing them with accessible credit alternatives. As noted, 25 million households in the U.S. remain unbanked or underbanked, highlighting a critical opportunity for financial inclusion through innovative payment solutions.

- Consumer Behavior Shift: Statistics indicate that 67% of consumers would use BNPL services more if they were widely available, with a notable preference among Gen Z and Millennials for such options. This demographic shift could lead to increased adoption of Cash App as a primary financial tool.

Key Challenges

- Financial Overextension Risks:

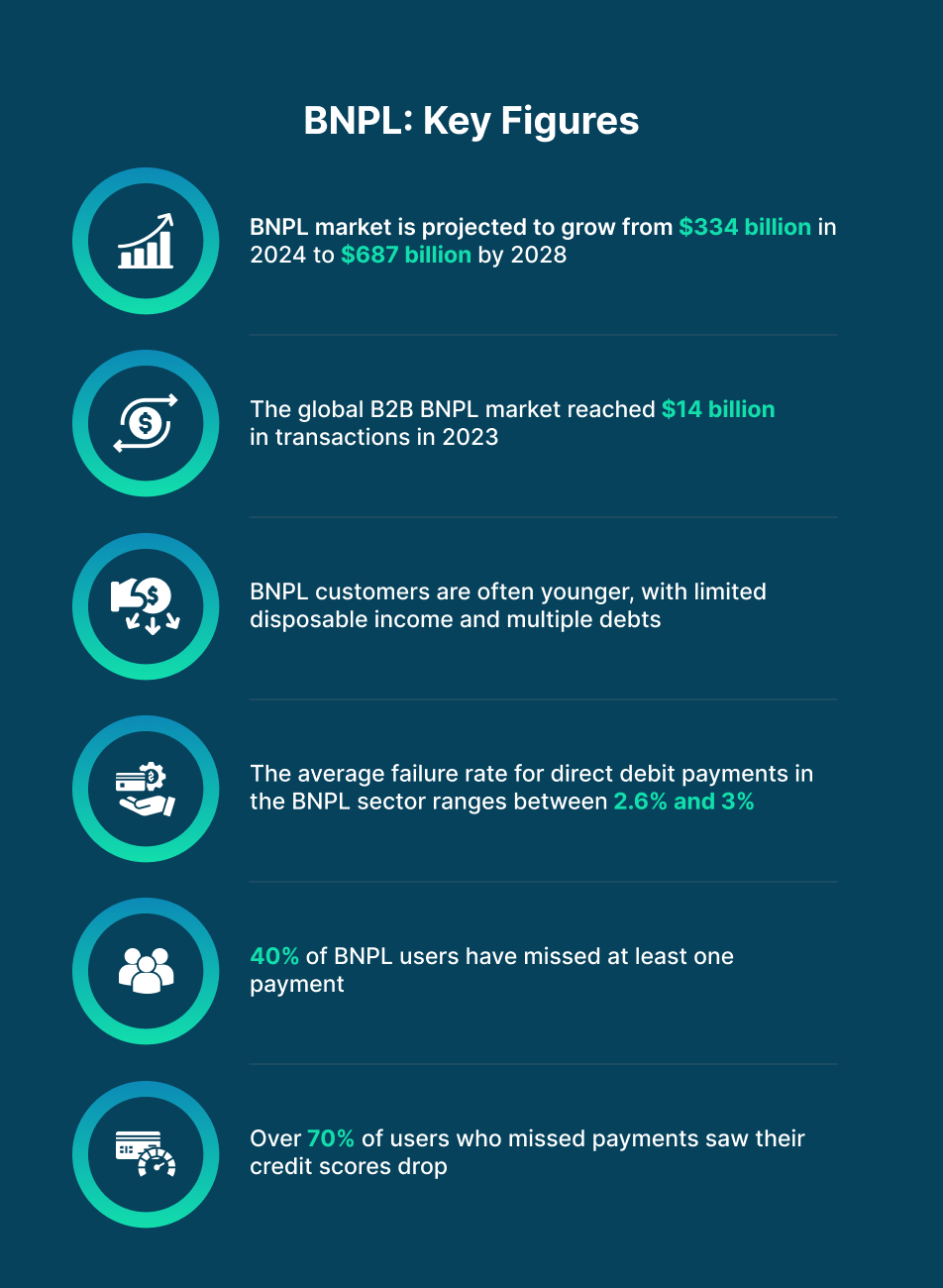

An area of concern with BNPL services is the risk of users over-extending themselves financially. 66% of users perceive BNPL as risky for accumulating unmanageable debt. This is concerning, given the fact that 34% of U.S. BNPL users have reported falling behind with one or more payments which eventually leads to late fees and negative credit scoring..

Furthermore, the BNPL market is projected to grow significantly, with an estimated total payment value of $80.77 billion by the end of 2024. As this market expands, the likelihood of consumer debt snowballing through BNPL transactions also increases.

Critics argue that unless safeguards are put in place, many will underestimate their financial obligations because BNPL transactions are usually unaccounted for in credit reporting agencies. Such invisibility complicates payment reconciliation and subsequently drives consumer financial stress.

- Cybersecurity and Data Privacy Concerns:

As digital payment ecosystems such as Cash App continue to evolve, cybersecurity and data privacy come to the forefront. BNPL transactions are sensitive to managing user data, and any breach could undermine user trust. That is why it's critical to ensure the security and absence of errors in payment reconciliation processes that maintain trust among consumers.

The spread of cyber attacks in the financial industry cannot be ignored. Indeed, reports indicate that three out of four shoppers utilized BNPL services in 2023. This widespread adoption creates a significant potential for fraud if robust security mechanisms are not in place. Strengthening safety measures will be crucial, particularly as Cash App integrates Afterpay's services.

Opportunities for Payment Reconciliation

Despite these challenges, the integration of Afterpay into Cash App offers significant opportunities for improving payment reconciliation processes:

- Enhanced Visibility and Control: Cash App enables instant payment reconciliation, addressing concerns about financial overextension. It provides users with clear visibility into their outstanding balances and upcoming payments. This transparency helps consumers manage their spending effectively and avoid exceeding their budgetary limits.

- Market Growth Potential: The BNPL market is growing rapidly, with an expected compound annual growth rate of around 40% from 2024 to 2032. That growth provides a perfect opportunity for Cash App to gain more grounds of this market by taking in the consumers seeking flexibility in payments. With an increase in the number of retailers embracing BNPL solutions, Afterpay will position Cash App at the forefront of this arena.

- Consumer Education Initiatives: To counter such risks that arise with the use of BNPL, Cash App has an opportunity to offer consumer education programs focused on responsible borrowing practices. In this direction, Cash App can provide budgeting and debt management resources along with its reconciliation tools to users for more informed financial decision-making.

A Step Toward Financial Equality

Dorsey's vision goes beyond integrating Afterpay with Cash App. He wants Cash App to be a broad banking solution for younger and lower-income users. This will be achieved as Block can position itself as a leader in the fintech space by fostering an ecosystem where payment reconciliation is seamless and intuitive.

The potential for growth is immense since Cash App has 57 million active users, with about 40% of these utilizing the Cash App Card. The more people subscribe to these services, the more Block's customer loyalty and retention improve together with higher transaction volumes.

This move signifies a shift in the financial landscape, prioritizing accessibility and simplicity. With Afterpay on 24 million Cash App cards, Jack Dorsey’s Block is not just creating a product—it’s fostering a movement. By championing payment reconciliation and accessible lending, this partnership has the potential to redefine how Americans interact with their money.

As we watch this integration unfold, one thing is clear: the era of digital finance isn’t just about innovation; it’s about inclusion. Payment reconciliation will undoubtedly play a pivotal role in ensuring the success of this ambitious venture, bridging gaps, and building trust in an increasingly cashless society.