What is Payment Reconciliation and How Does it Work?

Payment reconciliation is the process of matching payment records across payment gateways, banks, billing systems, and accounting ledgers to confirm that every transaction is accurately recorded and settled. This matching was traditionally done manually in spreadsheets, but growing transaction volumes have pushed finance teams toward automated tools that can perform reconciliation at scale.

In modern finance environments, payment reconciliation is no longer a back-office accounting task but a critical finance operations function that spans ERPs, payment gateways, banks, billing platforms, and settlement systems. As transaction volumes grow across channels, currencies, and geographies, finance teams must continuously align internal records with external payment data arriving in different formats and timelines. Payment reconciliation becomes complex not because of accounting rules, but because of operational realities—multi-source data, settlement delays, gateway fees, missing references, and ERP posting logic. For enterprises handling thousands of daily transactions, payment reconciliation directly impacts financial data integrity & accuracy, reporting integrity, audit readiness, and cash visibility across systems.

Payment Reconciliation in Modern Business Operations

As transaction volumes grow and payment methods multiply—from digital wallets to Buy Now Pay Later (BNPL) schemes—automated reconciliation becomes not just convenient, but essential for financial accuracy and operational efficiency. Businesses today process payments through dozens of channels, creating unprecedented complexity that manual processes simply cannot handle at scale, which is why finance teams increasingly turn to payment reconciliation software to manage multi-channel matching automatically.

Why is Payment Reconciliation Important?

Payment reconciliation holds significant importance for businesses for several compelling reasons:

Financial Accuracy and Reliability

Accurate financial records are crucial for reliable financial reporting, budgeting, and decision-making. Payment reconciliation ensures that all payments received are accurately recorded, providing a reliable basis for understanding the company's financial position. Without proper reconciliation, businesses operate with incomplete or incorrect financial data, leading to poor strategic decisions and potential financial losses.

Modern businesses require real-time visibility into their cash position. Reconciliation provides this clarity by ensuring every dollar received is properly accounted for and matched to the corresponding invoice or transaction record.

Fraud Detection and Prevention

Regular reconciliation helps detect and prevent fraudulent activities. By verifying that payments received match those recorded in the financial system, businesses can identify unauthorized or suspicious transactions early and take corrective action to mitigate potential losses.

Payment fraud costs businesses billions annually. Automated reconciliation systems use pattern recognition and anomaly detection to flag suspicious transactions that might indicate fraud, unauthorized access, or data breaches. Early detection through systematic reconciliation can prevent minor issues from escalating into major financial losses.

Regulatory Compliance

Compliance with financial regulations is essential for businesses. Payment reconciliation helps ensure that the company maintains accurate and transparent financial records, reducing the risk of non-compliance with regulatory requirements and associated penalties.

Organizations subject to SOX compliance, PCI DSS standards, GDPR requirements, or industry-specific regulations must demonstrate robust internal controls. Payment reconciliation provides the documentation and audit trail necessary to prove compliance during regulatory examinations and financial audits.

Improved Cash Flow Management

Accurate reconciliation provides insights into the company's cash flow, facilitating effective cash flow management. It helps in monitoring incoming payments, managing liquidity, planning for future cash needs, and avoiding cash shortages.

Understanding exactly when payments clear, identifying delayed transactions, and recognizing payment patterns enables businesses to forecast cash flow more accurately. This visibility supports better working capital management, reduces the need for emergency financing, and improves overall financial stability.

Enhanced Customer Relations

Accurate reconciliation ensures that customer payments are correctly recorded and applied to their accounts. This reduces the likelihood of billing errors and disputes, enhancing customer satisfaction and trust in the company's financial practices.

Nothing damages customer relationships faster than incorrect billing or misapplied payments. When customers pay invoices but continue receiving collection notices due to reconciliation errors, it creates frustration and damages trust. Proper reconciliation ensures customers receive accurate account statements and appropriate credit for their payments.

Operational Efficiency

Automated reconciliation tools streamline the reconciliation process, reducing manual effort and increasing efficiency. This allows businesses to allocate resources more effectively and focus on core operations, improving overall operational productivity.

Finance teams spend countless hours on manual reconciliation when they could be performing strategic financial analysis. Automation reduces Payment reconciliation time by 70-90%, freeing staff to focus on exception handling, process improvement, and value-added financial planning activities.

Informed Decision-Making

Reliable financial records provide a solid foundation for strategic decision-making. Businesses can use accurate payment reconciliation data to make informed decisions about investments, growth opportunities, and other financial matters.

Executives making decisions about expansion, acquisitions, or major investments need confidence in their financial data. Proper reconciliation ensures that reported revenue, accounts receivable, and cash positions accurately reflect reality, supporting better strategic planning and risk management.

What does Payment Reconciliation mean in Finance

In enterprise environments, payment reconciliation does not live inside accounting alone. It operates across multiple operational systems where transaction data originates, transforms, and finally lands in financial records. Finance teams are required to correlate inputs from:

- Payment gateways and processors generating transaction and settlement data

- Bank statements and settlement reports reflecting actual fund movement

- ERP and accounting ledgers where entries are recorded

- Billing, subscription, or invoicing platforms creating payment expectations

- Internal order management or invoice systems tracking receivables

The same transaction is represented differently across these systems.

- Timestamps vary between authorization, capture, and settlement stages

- Reference IDs may be missing, inconsistent, or formatted differently

- Gateway fees and charges are deducted before settlement amounts reach the bank

- Foreign exchange conversions alter final settled values

- Partial captures, refunds, and chargebacks further fragment transaction visibility

Because of these variations, finance teams must continuously validate whether:

- The expected amount to be received matches what was actually settled

- The settled amount matches what is recorded in the ERP

- System mismatches are not silently creating ledger discrepancies over time

Payment reconciliation therefore acts as a core operational control that preserves financial data integrity, supports reliable reporting, and prevents cross-system inconsistencies from turning into accounting risks.

Why Payment Reconciliation Is Operationally Complex in Modern Finance

The complexity of payment reconciliation in modern enterprises stems from how payments travel through disconnected systems before they ever reach the ledger. What appears as a single customer payment is, in reality, fragmented across platforms that record different stages of the same transaction.

A typical payment may:

- Originate through a payment gateway or processor

- Be recorded in a billing or subscription platform as a successful charge

- Appear days later inside a bank settlement or payout report

- Be posted separately as an entry inside the ERP or accounting system

- Reflect deductions for gateway fees, taxes, currency conversion, or chargebacks

These records do not arrive at the same time or in the same structure.

- Settlement files are delayed and often batch multiple transactions into one payout

- Banks show net credits without transaction-level breakdowns, and the global payments industry continue to fragment as new rails and ecosystems emerge.

- Reference IDs differ or are missing across systems

- Partial captures, refunds, and split settlements distort one-to-one matching

- Multi-currency transactions change values between authorization and settlement

As a result, finance teams are forced to interpret:

- Timing gaps between transaction, settlement, and posting

- Hidden fee deductions not visible inside ERP records

- Data format inconsistencies between gateway, bank, and ERP exports

Payment reconciliation becomes operationally complex not because of accounting rules, but because financial truth is scattered across fragmented operational data sources.

How does the Payment Reconciliation Process work?

Enterprise payment reconciliation follows a disciplined operational workflow designed to bring consistency across gateways, banks, ERP systems, and billing platforms. While tools may vary, the underlying process remains structured and repeatable to ensure financial accuracy at scale.

1. Data Collection

Transaction and settlement data is gathered from multiple sources: payment gateways, bank statements, ERP ledgers, billing or subscription systems, and internal order platforms. Each source reflects a different stage of the same payment lifecycle.

2. Data Normalization

Formats are standardized across files and systems. Currencies, timestamps, reference fields, payout structures, and transaction descriptors are aligned to enable reliable comparison.

3. Transaction Matching

Records are matched using invoice numbers, order IDs, payment references, customer IDs, or rule-based logic. Exact, partial, and tolerance-based matches are applied depending on data quality.

4. Fee and Deduction Handling

Gateway fees, processing charges, taxes, foreign exchange differences, and chargebacks are identified so that gross transactions can be reconciled with net settlements.

5. Exception Identification

Unmatched, partially matched, duplicate, or inconsistent transactions are automatically flagged for review.

6. Exception Resolution

Finance teams investigate timing differences, missing references, split settlements, refunds, or data gaps across systems to resolve discrepancies.

7. Ledger Update

Validated transactions and adjustments are accurately posted or corrected inside the ERP or accounting system.

8. Reporting and Verification

Reconciliation summaries and audit-ready reports are generated for internal controls, compliance checks, and financial verification.

This end-to-end payment reconciliation process runs daily or weekly based on transaction volume and business model complexity.

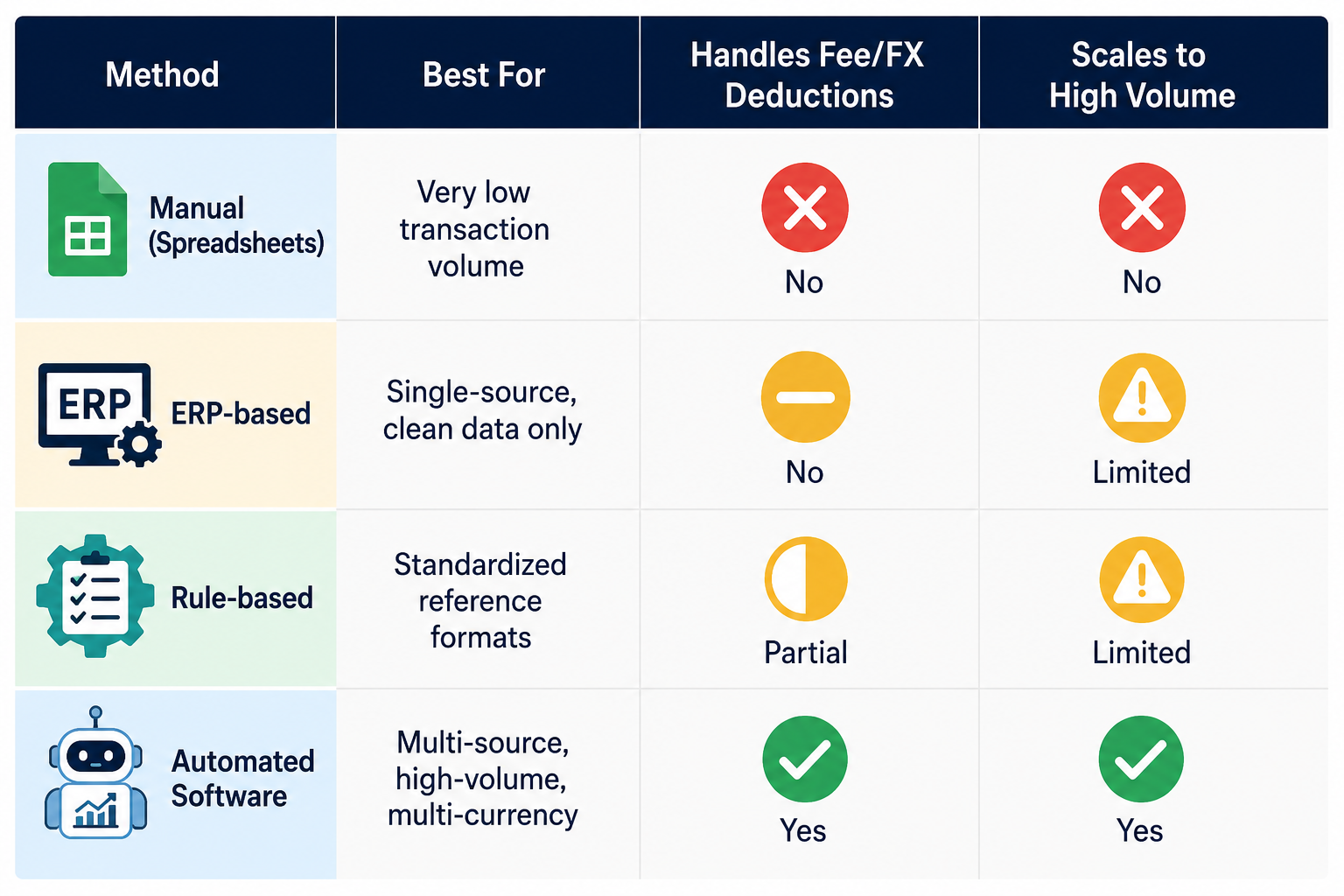

Methods of Payment Reconciliation

Organizations adopt different methods for payment reconciliation depending on transaction volume, system maturity, and operational complexity.

Manual Reconciliation

- Spreadsheet-based comparison of gateway reports, bank statements, and ERP records

- Human verification of transaction references, amounts, and dates

- Heavy dependency on individual knowledge and effort

- Suitable only for very low transaction volumes or single-channel payments

ERP-Based Reconciliation

- Limited matching capabilities within accounting or ERP modules

- Works only when incoming data follows consistent structure and references

- Cannot interpret gateway settlement reports, fee deductions, or timing gaps

- Assumes data entering the system is already accurate

Rule-Based Reconciliation

- Uses predefined logic to match transactions based on reference fields

- Reduces repetitive manual effort for standard scenarios

- Struggles when references are missing, inconsistent, or split across systems

- Requires frequent rule maintenance as payment channels evolve

Automated Reconciliation Systems

- Ingest data from gateways, banks, ERPs, and billing platforms

- Apply intelligent matching across inconsistent formats and references

- Handle fee deductions, FX differences, and partial settlements

- Manage exceptions through structured workflows at scale

As modern payment ecosystems expand across gateways, currencies, and systems, organizations naturally transition from manual and ERP-dependent approaches toward automated reconciliation to maintain control and accuracy.

Types of Payment Reconciliation

Payment reconciliation can take different forms depending on transaction sources, financial systems, and business models. Most enterprises perform multiple types of reconciliation to ensure accurate financial reporting and clean cash flow tracking.

Where Manual Reconciliation Breaks at Scale

Manual payment reconciliation may work when transaction volumes are low and data sources are limited. However, as organizations grow, the number of gateways, bank accounts, settlement files, currencies, and internal systems increases rapidly, making spreadsheet-based reconciliation unsustainable.

Finance teams begin relying on exported CSV files, VLOOKUPs, pivot tables, and human verification to compare transactions across systems. What starts as a manageable daily task turns into hours of repetitive effort with rising chances of oversight. Timing gaps between transaction dates and settlement dates require constant interpretation. Fee deductions, FX adjustments, split payouts, and missing references force teams to manually investigate records line by line.

As volumes scale into thousands or millions of transactions per month, manual processes introduce:

- High risk of human error and missed discrepancies

- Delays in closing books and generating accurate reports

- Difficulty tracking exceptions across multiple files and versions

- Increased audit stress due to lack of traceability and control

- Dependency on individual team members’ spreadsheet knowledge

Manual payment reconciliation does not fail because finance teams lack skill. It fails because operational complexity outgrows what spreadsheets and human comparison can reliably handle at enterprise scale. This is the point where finance operations require structured systems rather than spreadsheet-driven effort to sustain reconciliation accuracy.

Role of ERP & Accounting Systems in Reconciliation

ERP and accounting systems like SAP, NetSuite, and Microsoft Dynamics play an important role in recording financial transactions, maintaining ledgers, and supporting reporting. They are designed to ensure accounting accuracy once transactions are validated and posted. However, they are not built to perform end-to-end payment reconciliation across multiple external data sources.

ERPs primarily rely on structured journal entries and predefined data fields. They expect clean, consistent inputs. In real payment environments, data arrives from gateways, banks, and billing platforms in varied formats, often with missing or inconsistent references. Settlement files may show net credits, while ERPs require transaction-level detail. Gateway fees, FX differences, and split payouts are not always visible in a format that ERPs can interpret automatically.

Because of this, finance teams often export data out of the ERP into spreadsheets to perform reconciliation before updating the ledger.

ERPs support reconciliation after validation, but they do not handle:

- Multi-source data ingestion

- Complex transaction matching logic

- Exception identification across systems

- Interpretation of settlement and fee structures

This creates ERP Reconciliation challenges that ERPs alone cannot bridge. This limitation is what forces finance teams to rely on external processes before transactions can be safely recorded in the ledger.

Why Automated Payment Reconciliation Becomes Necessary in High-Volume Environments

As transaction volumes grow, payment reconciliation automation shifts from a manageable task to a continuous operational burden. What may work with dozens of daily transactions becomes unsustainable when finance teams must reconcile thousands of records flowing from gateways, banks, ERPs, and billing platforms every day.

Manual reviews, spreadsheet comparisons, and ERP exports cannot keep pace with the speed, volume, and variability of modern payment data. Settlement delays, fee deductions, split payouts, and inconsistent references create a growing queue of exceptions that demand attention. Over time, finance teams spend more effort identifying mismatches than validating financial accuracy.

Automation becomes necessary not for convenience, but for operational continuity. It allows organizations to process large volumes of payment data reliably without increasing manual workload or risking reconciliation backlogs.

Automated reconciliation enables:

- Continuous ingestion of multi-source data

- Standardization of formats across systems

- Accurate transaction matching at scale

- Faster identification of exceptions

- Consistent reconciliation cycles despite growing complexity

In high-volume environments, automation is what keeps payment reconciliation aligned with business velocity. Many enterprises adopt specialized platforms like Optimus Payment Reconciliation to handle this scale reliably.

Best Practices and Core Capabilities of a Modern Payment Reconciliation System

An effective payment reconciliation system must go beyond basic matching and support the operational realities of enterprise finance. As data flows in from gateways, banks, ERP systems, and billing platforms, the system must be capable of handling differences in structure, timing, and references without constant manual oversight.

Key capabilities include:

- Multi-source data ingestion from payment gateways, bank statements, ERP ledgers, and billing systems

- Data normalization to standardize formats, currencies, timestamps, and reference structures

- Flexible matching logic using invoice numbers, order IDs, payment references, and configurable rules

- Fee and deduction handling for gateway charges, FX differences, and net settlements

- Exception management workflows to identify, categorize, and route mismatches for resolution

- Audit trails and controls to maintain transparency and compliance for finance reviews

- Scalability to process growing transaction volumes without performance impact

- Configurable rules to adapt to different business models and settlement patterns

These capabilities ensure that payment reconciliation remains reliable, controlled, and efficient even as operational complexity increases across systems.

Key Metrics Finance Teams Track in Payment Reconciliation

To keep payment reconciliation effective and controlled, finance teams rely on specific operational metrics that reflect accuracy, speed, and financial integrity across systems. These metrics help identify gaps early, reduce reconciliation backlogs, and maintain confidence in financial reporting.

Key metrics commonly tracked include:

- Reconciliation rate — percentage of transactions successfully matched across systems

- Exception rate — volume of unmatched or partially matched transactions requiring review

- Time to reconcile — average time taken to complete reconciliation for a settlement cycle

- Aging of exceptions — how long discrepancies remain unresolved

- Settlement accuracy — validation of expected vs. actual credited amounts after fees and deductions

- Fee variance tracking — monitoring gateway charges, FX impacts, and processing deductions

- Ledger posting accuracy — correctness of entries reflected in ERP and accounting records

- Audit readiness — availability of audit-ready reconciliation reports and traceability for financial reviews

- Impact on DSO — how reconciliation delays affect receivables visibility and cash flow clarity

Tracking these metrics ensures payment reconciliation remains measurable, transparent, and aligned with enterprise finance control objectives.

How Optimus Enables Intelligent Payment Reconciliation

To address these operational challenges, organizations adopt intelligent reconciliation platforms designed specifically for multi-system finance environments.

Optimus Payment Reconciliation is a purpose-built to handle the operational complexity of payment reconciliation across enterprise systems without adding manual overhead to finance teams. It connects with payment gateways, banks, ERP systems, billing platforms, and internal data sources to create a unified reconciliation environment.

Key ways Optimus enables intelligent payment reconciliation include:

- Multi-source data ingestion from gateways, bank statements, ERP, and billing systems in native formats

- Data normalization to standardize timestamps, currencies, references, and transaction structures

- Advanced matching logic using invoice IDs, order references, payment IDs, and configurable rules

- Automated fee and deduction handling for gateway charges, FX differences, and processing costs

- Real-time exception identification for unmatched, partially matched, or mismatched transactions

- Workflow-driven exception resolution with audit trails and ownership tracking

- ERP-ready outputs to ensure accurate ledger posting without manual adjustments

- Reconciliation dashboards and reports for audit, compliance, and finance visibility

By combining automation, intelligent matching, and operational workflows, Optimus allows finance teams to reconcile high volumes of transactions with accuracy, speed, and full traceability—turning payment reconciliation from a manual burden into a controlled financial process. Request a demo with Optimus today!

Frequently Asked Questions on Payment Reconciliation

What is payment reconciliation in accounting?

Payment reconciliation is the process of verifying that transactions recorded across gateways, banks, billing systems, and ERP ledgers align accurately in amount, reference, and settlement status.

What is the difference between bank and payment reconciliation?

Bank reconciliation compares ledger balances with bank statements. Payment reconciliation goes further by validating transaction-level data across gateways, settlement files, ERP entries, and billing records.

What is automated payment reconciliation?

Automated payment reconciliation uses software to ingest data from multiple systems, standardize formats, apply matching logic, and identify exceptions without manual spreadsheet comparison.

How is payment reconciliation different in multi-gateway, multi-ERP environments?

Multiple gateways and ERPs create inconsistent references, varied settlement timelines, and fragmented data formats, increasing the complexity of matching transactions accurately across systems.

What operational steps are involved in an enterprise payment reconciliation process?

The process typically includes data collection, normalization, transaction matching, fee adjustment, exception handling, ledger updates, and reporting for audit verification.

What methods do finance teams use to reconcile payments across systems?

Teams rely on spreadsheets, limited ERP matching, rule-based tools, or specialized automated reconciliation platforms depending on transaction volume and complexity.

What limitations do ERP and accounting systems have in handling payment reconciliation?

ERPs lack the ability to interpret gateway settlements, fee deductions, timing gaps, and cross-system references needed for complete reconciliation.

What are the most common sources of discrepancies in payment reconciliation?

Timing differences, missing references, fee deductions, partial settlements, currency conversions, and inconsistent data formats frequently cause mismatches.

You can reach us at:

1700 Montgomery St, San Francisco, California 94111

6470 E Johns Crossing Suite 160, Johns Creek, GA 30097

Copyright © 2026 Optimus. All Rights Reserved.