Did you know that fintechs and PSPs lose up to 1.5% of annual revenue to hidden payment discrepancies and inefficiencies, according to Forrester? Why are payment costs still bleeding margins dry in 2025 that too despite tech advances? With transaction fees skyrocketing across PSPs, banks, and networks, plus compliance headaches under PSD3 and PCI DSS 4.0, finance teams face a brutal squeeze. The winners? Those wielding AI-powered automation to slash leakage, reclaim profits, and turn payments into a growth engine. Want to explore more? Let's deep dive.

Core Payment Cost Challenges for Fintechs and PSPs

Traditional PSP business models primarily focused on just moving money are increasingly under pressure. Merchants demand more value-added services such as embedded finance, analytics, and enhanced customer experiences, further squeezing gross margins. The typical PSP fee ranges from 2.5% to 3.5% per transaction plus fixed fees, while banks often impose up to 6.2% on cross-border transactions due to foreign exchange and settlement complexity. Card network interchange fees add another 1.5% to 2.5% cost, varying by card type and geography. Collectively, these layers can consume more than 10% of transaction value in some international scenarios, considerably reducing net revenue for fintech operators and merchants.

Complicating matters are regulatory requirements such as the European Union’s PSD3 directive and PCI DSS 4.0 compliance, which increase operational costs by approximately 25% for multinational PSPs and fintechs. Siloed data from fragmented payment providers combined with manual reconciliation processes creates operational bottlenecks, with 60% of finance teams spending over 10 hours weekly on error-prone reconciliation tasks. These inefficiencies not only inflate staffing costs but also delay financial closes and elevate the risk of compliance penalties.

Hidden Revenue Drains and Fee Leakage

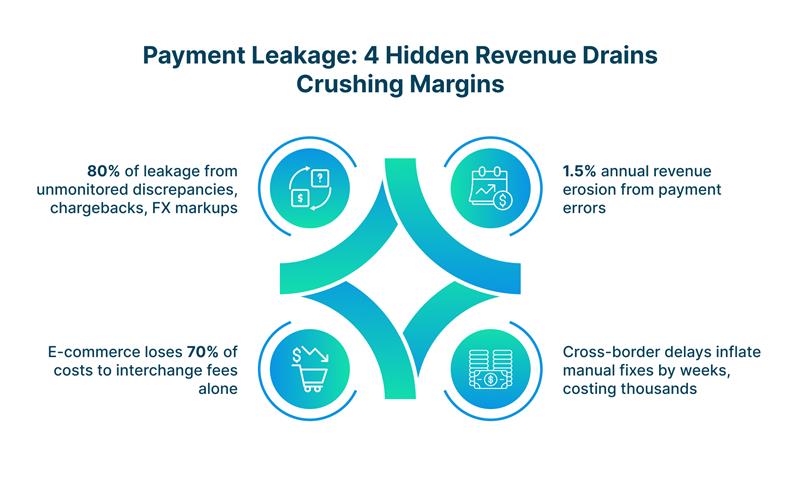

Beyond visible fees, fintechs and PSPs face a silent margin-erosion problem from hidden revenue leakage. Up to 80% of leakage stems from unmonitored discrepancies, chargebacks, FX markup margins, and failed transactions that go undetected due to fragmented payment ecosystems. For example, e-commerce firms see roughly 70% of their costs driven by interchange fees, yet they frequently fail to capture lost fees from failed or duplicated settlements.

Operational silos prevent comprehensive fee analysis and fraud detection, culminating in an estimated 1.5% of revenue lost annually to payment discrepancies and errors, according to Forrester Research. Complex cross-border workflows heighten this challenge, as currency conversions, delayed dispute resolution, and inconsistent audit trails prolong error detection by weeks, inflating manual investigation and correction workloads.

A breakdown of typical payment costs for a company processing $10 million yearly illustrates the scale of these challenges: