Fee discrepancies that are related to payment reconciliation errors continue to be an operational and financial drain on organizations everywhere. In fact, almost 40% of the finance team’s time is spent on manual, inefficient reconciliation, resulting in potential losses of close to 0.5% of the year’s revenue from inefficiencies/delays on settlement. If that’s not bad enough, it’s estimated that 62% of companies are still using spreadsheets to perform their reconciliation, which puts them at significant risk of both errors and delays in reporting, creating challenges in managing compliance and cash flow. For CFOs, intelligent payment reconciliation safeguards profitability and efficiency—but building effective solutions requires more than just better systems or software.

Payment Reconciliation: The cornerstone of strategic CFO leadership

As the amount of information is increasing frequently and at a diverse pace, it’s now imperative for CFOs to implement solutions to efficiently track, reconcile, and maintain financial integrity for a variety of transactions. This allows them to reduce errors, improve compliance, manage cash flow, and minimize risk exposure while identifying strategic opportunities in today’s increasingly complex financial landscape.

A 2025 Trullion study found 73% of auditors still rely heavily on spreadsheets for reconciliations, data extraction, and outdated processes—leading to inefficiencies and higher error risk. Nearly 50% cited reconciliations as their biggest challenge, taking 5–20 hours weekly and delaying financial close. Despite automation potential, only one-third use AI. For CFOs, resolving fee discrepancies remains critical for profitability, compliance, and streamlined financial operations.

Reconciliation Insights: A closer look at fee discrepancies

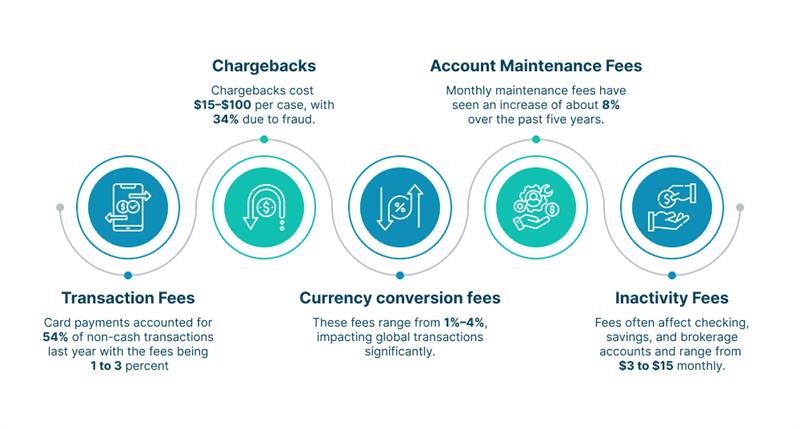

- Transaction fees: Card payments accounted for 54% of non-cash transactions last year with the fees being 1 to 3 percent.

- Chargebacks: Chargebacks cost $15–$100 per case, with 34% due to fraud.

- Currency conversion fees: These fees range from 1%–4%, impacting global transactions significantly.

- Account maintenance fees: Monthly maintenance fees have seen an increase of about 8% over the past five years.

- Inactivity fees: fees often affect checking, savings, and brokerage accounts and range from $3 to $15 monthly

These discrepancies occur when the fees charged or recorded do not match the actual fees incurred or agreed upon. These discrepancies arise from several sources: