Top 5 Challenges in Cash Reconciliation and How to Overcome Them: “Friends” Discuss

John Tribbiani, once a struggling actor, is now a successful star with his own thriving production company. But lately, John's been pretty frustrated. He's having a hard time tracking the cash transactions recorded in his company's financial records and matching them with the actual cash on hand or in the bank. John's been scratching his head, trying to figure out how to make the numbers line up. Naturally, he's turned to his savior, Edward Bing—the one friend in their group who actually understands financial management.

Edward and John are sitting at Central Perk, sipping their coffees. John is curious about what Edward has to say about his situation or rather the solution to his financial woes. Edward after listening to John takes the sip of his coffee and…..

Edward : So John, have you ever heard of the term cash reconciliation.

John : Cash, What?

Edward : Well, let's say cash reconciliation is something you need for your business right now. It will ensure that your cash balances in the financial records match the actual cash on hand.

John : Okay, got it. But why is it so important, Edward?

Edward : Well, it’s fundamental to maintaining financial integrity. But hey, it's also filled with challenges that can lead to discrepancies, inefficiencies, and frustration.

John : Oh No, What kind of challenges are we talking about?

Edward : For starters, there's human error. Like you, people make mistakes when recording transactions. Then, there are delays in recording transactions, which can mess up the balances.

John : Sounds annoying. What else?

Edward : Fraud is another big one. Someone might be pocketing cash and covering it up. Then there are system mismatches, where the accounting software doesn’t sync up with actual cash records. And don't forget complex reconciliation processes that are just hard to manage.

John : Wow, that’s a lot. What happens if these challenges aren't fixed?

Edward : You could end up with inaccurate financial reporting, loss of funds, and increased operational costs. Not exactly a good situation for any business.

John : Yikes! So, what can businesses do to fix these issues?

Edward : Glad you asked. Understanding these obstacles is the first step. Then, implementing practical solutions can significantly improve the accuracy and efficiency of cash reconciliation.

John : Like what kind of solutions?

Edward : Things like automating the reconciliation process, improving staff training, using better software, conducting regular audits, and simplifying the processes can help a lot.

John : Sounds like a plan. So, it’s all about making the process smoother and more reliable, right?

Edward : Exactly. By addressing these challenges, businesses can ensure smoother financial operations and enhance trust in their financial management.

John : Edward, can you be a bit more clear and simple, I do not have the Thesaurus with me to understand these complex words!

Edward : Could I be more, Clear or SImple !!!!!!

Well, here are the top five challenges in cash reconciliation and explore effective strategies to overcome them in detail.

Let’s Explore!!!

1. Data Entry Errors

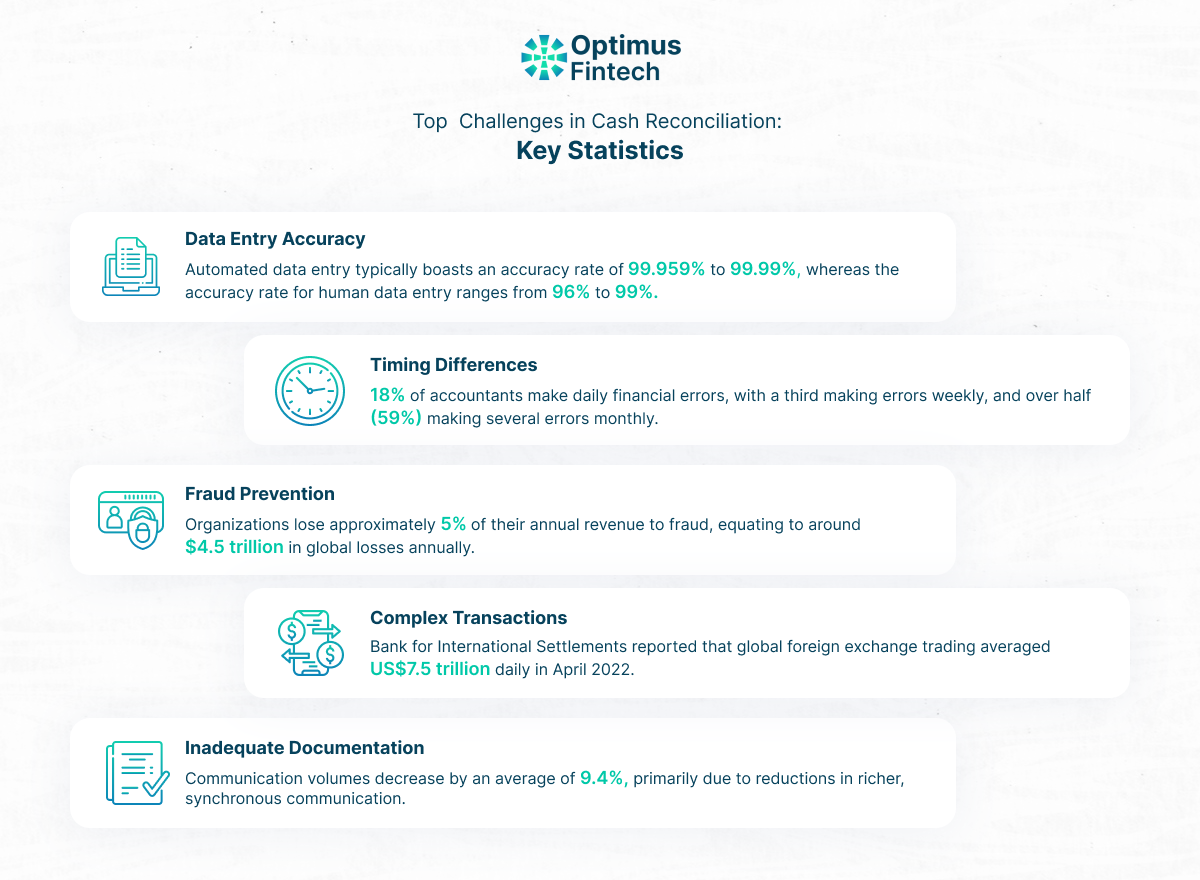

John, “as someone who works in statistical analysis and data reconfiguration, I can tell you, humans make way more data entry mistakes than automated systems do. For example, statistics show that automated data entry typically boasts an accuracy rate of 99.959% to 99.99%, whereas the accuracy rate for human data entry ranges from 96% to 99%. As a result, data entry errors remain one of the most common issues in cash reconciliation. These errors can range from simple typos to recording incorrect amounts, which can disrupt the entire reconciliation process.”

Solution: “Automate your data entry wherever possible. Using accounting software with integrated bank feeds can significantly reduce the risk of human error. Additionally, regular training for staff on accurate data entry practices can help minimize mistakes.”

2. Timing Differences

John, the second challenge is time differences. Remember how I was stuck in Tulsa on Christmas Eve while you were already home?

“Yeah Edward, I do remember you were still at the office with the former Miss Oklahoma runner-up.”

Exactly! What!!!!!!!!

“No John, we were in office because Tulsa is an hour behind New York. Time differences can really complicate things.”

Yeah John, and the same applies to offices located across the globe. Did you know a recent Gartner survey found that 18% of accountants make daily financial errors, with a third making errors weekly, and over half (59%) making several errors monthly. Timing discrepancies significantly distort financial statements, impacting the accuracy of revenue recognition, expense reporting, and balance sheet reconciliation. Timing differences occur when transactions are recorded at different times in your books and on your bank statements. For instance, a deposit made late in the day might not appear on the bank statement until the next day, causing temporary discrepancies.

Solution: Maintain a detailed record of your transactions and categorize them by date. Reconcile your accounts daily or weekly rather than monthly to keep timing differences minimal. Most importantly, communicate with your bank to understand their processing times for different types of transactions.

3. Internal Controls and Fraud Prevention

"Do you remember, John, when a woman stole Monica's credit card and her identity?"

“Oh yeah, Monica ended up liking her and even became friends with her.

“Well, yeah, but in reality fraudsters are not your “friends” in fact payment fraud is a significant and growing concern worldwide. Juniper Research predicts that global online payment fraud losses will surpass $362 billion in the next five years. The Association of Certified Fraud Examiners (ACFE) reports that organizations lose approximately 5% of their annual revenue to fraud, equating to around $4.5 trillion in global losses annually. When internal controls are inadequate, businesses are vulnerable to various forms of fraud, including misappropriation of funds, unauthorized transactions, and falsified records. These issues can go unnoticed during the reconciliation process, resulting in financial discrepancies and potential regulatory non-compliance.”

Solution: Strengthen internal controls by segregating duties and implementing dual approval processes for significant transactions. Conduct regular audits and reconcile accounts independently to detect and prevent fraudulent activities.

4. Complex Transactions

“John, just like life, financial transactions can be complex too. You will be surprised to know that the Bank for International Settlements reported that global foreign exchange trading averaged US$7.5 trillion daily in April 2022. These transactions, which include international payments and multi-currency transactions among multiple parties, are often complex and lengthy, spanning several days. This complexity can complicate the reconciliation process and increase the likelihood of errors. But do not worry John, there is a solution to this problem.”

Solution: Use specialized software that can handle complex transactions and multi-currency accounting. Ensure your staff is well-trained in managing these types of transactions. Breaking down complex transactions into smaller, more manageable parts can also simplify the reconciliation process.

5. Inadequate Documentation

“The last but not least challenge is cross-border communication”. You know John, cross-border communication costs have decreased, making global work distribution easier, but geographical distance still presents challenges. Research indicates that as temporal distance increases, total communication volumes decrease by an average of 9.4%, primarily due to reductions in richer, synchronous communication. Effective coordination with banking partners is crucial for optimizing the reconciliation process. In larger organizations, different departments or teams managing cash transactions can result in communication gaps and inconsistencies in reporting.

Solution: Promote cross-departmental communication with shared access to reconciliation tools and regular meetings to keep teams aligned. Clear documentation of reconciliation procedures ensures consistency, streamlines operations, and reduces errors in financial reporting. Regular updates and training sessions enhance understanding and foster a cohesive approach to cash management and reconciliation.

Edward these are some really alarming challenges, and solutions seem to be fitting but anything else you want me to know about this:?

“Well John, Yes in deed there is something”

Overcoming These Challenges: A Proactive Approach

- Leverage Technology: Invest in reliable accounting software that offers features such as automated bank feeds, real-time payment reconciliation, and error detection. Technology can greatly reduce manual effort and the potential for errors.

- Regular Training: Keep your staff updated with regular training sessions on best practices in cash reconciliation. A well-informed team is less likely to make mistakes and is more capable of identifying and addressing issues promptly.

- Establish Clear Procedures: Develop and document clear, step-by-step procedures for cash reconciliation. Standardized processes help ensure consistency and can make it easier to identify and correct discrepancies.

- Conduct Frequent Reconciliations: Rather than waiting for month-end, reconcile your accounts daily or weekly. Frequent reconciliations allow you to catch and resolve issues before they escalate.

- Engage in Regular Audits: Regular internal audits can help identify weaknesses in your reconciliation process and ensure compliance with established procedures. Audits also provide an opportunity to update processes and technology as needed.

Final Thoughts

“So in summary, John the process of cash reconciliation can appear daunting, yet with effective strategies, tools, and a proactive mindset, you can simplify the process and conquer typical challenges. Like I mentioned, automating routine tasks such as transaction matching and data entry reduces manual errors and accelerates the reconciliation timeline. Maintaining meticulous records ensures accuracy, providing a clear audit trail for financial transactions.”

“But Hey, it is equally important to train your team so they stay updated on best practices and evolving technologies in financial management. You know what, by fostering a culture of consistency and attention to detail, you'll fortify your ability to keep financial records aligned with actual cash flow, thereby enhancing overall financial transparency and decision-making within your organization.”

“I hope now you have an idea about top Challenges in Cash Reconciliation and how to overcome them, and in case you have any questions, reach out to me, You know, I'll be there for you”