Commissions in the payment ecosystem are fees paid to processors, banks, and affiliates for facilitating a transaction. The four main types are Merchant Discount Rate (MDR), referral commissions, transaction commissions, and cross-border commissions, each calculated differently depending on transaction value, volume, and provider agreements.

Commissions are the fees that intermediaries - payment processors, banks, and affiliates, earn for helping a transaction move safely from a consumer's card to a merchant's account. This guide breaks down the different commission types, how they're calculated, and why they matter for any business that accepts digital payments.

The Payment Ecosystem: A Quick Overview

First and foremost, before we get started on comprehending commissions, let's take a quick look at the payments reconciliation environment. This is analogous to a sophisticated machine with multiple cogs, each of which contributes significantly to the smooth operation of the system. They include:

- Merchants: The sellers who offer goods or services.

- Consumers: The buyers who purchase those goods or services.

- Payment Processors: The entities that handle the processing of payment information.

- Acquiring Banks: The banks that maintain the merchant's account and receive the transaction amount.

- Issuing Banks: The banks that issue credit or debit cards to consumers.

- Card Networks: Entities such as Visa, MasterCard, and American Express that facilitate the flow of information and funds between banks.

They all work in perfect balance to make sure that your transaction completes swiftly whether you swipe your card or click "Pay Now." However like any well-oiled machine, maintenance is essential, and that's where commissions come in.

The Role of Commissions in the Payment Ecosystem

Ever wondered what actually happens behind the scenes when one makes a payment? Commission, in its essence, is a fee earned by intermediaries in a transaction, including payment processors, banks, and affiliates. In fact, such fees are generally a portion of the actual transaction amount, though they could be in the form of fixed rates as well. Commission structures also vary by industry, card network, and merchant risk profile, and they give these intermediaries an incentive to process your payments quickly and, more importantly, securely.

Commissions are at the heart of the payment ecosystem, ensuring money flows correctly and smoothly between banks, card networks, and payment processors. These fees will be laid out and explained below to show exactly how they work and why they matter for businesses and consumers alike.

Types of Commissions in Payments

In the general sense, commissions in the payment ecosystem represent some sort of fees for the services of intermediaries. These commissions may be devised in many ways in the context of the roles participants play and types of transactions involved in the payment ecosystem. Understanding these commission types is crucial in optimizing business payment processes and effective cost management. Many of these fee types can now be tracked and reconciled automatically, see how fees and commissions reconciliation works. Following are some of the key commission types in payments:

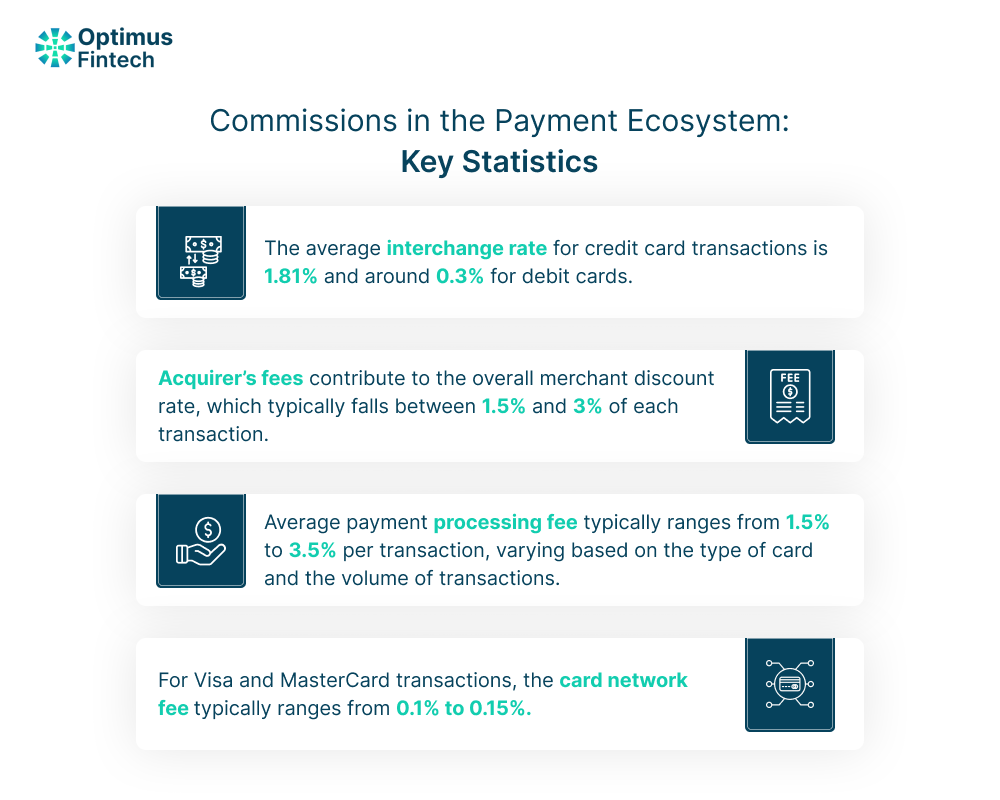

1. Merchant Discount Rate (MDR): This is a fee charged to merchants by payment processors for handling credit card transactions. It is typically a percentage of the transaction amount. The MDR includes the interchange fee, payment processor's fee, and other associated costs. According to recent statistics, the average MDR for credit card transactions ranges from 1 % to 3 % as of 2023, depending on the industry and card type.

2. Referral Commissions: These are the commissions paid to partners or affiliates referring customers to a payment service provider. They can come as a fixed amount per referral, or they can come as a share of revenue coming from the customer referred. Referral commissions have just become a huge business for many companies due to the recent rise of affiliate marketing in the world of Fintech.

3. Transaction Commissions: Payment processors often charge a small fixed fee per transaction in addition to the percentage-based MDR. For example, payment gateways might charge a fee of $0.25 per transaction, which can accumulate significantly for businesses with high transaction volumes.

4. Cross-Border Commissions: When a transaction involves currency conversion or international payments, additional commissions are often charged. These commissions can include a percentage of the transaction amount and a fixed currency conversion fee. In 2023, cross-border fees typically ranged from 1% to 3% of the transaction amount, depending on the payment provider, and card networks such as Visa and Mastercard separately levy their own currency-conversion assessment fees on top of this range.

Key Differences Between Fees and Commissions

While often used interchangeably, fees and commissions play distinct roles in the payment ecosystem. Understanding their differences is crucial for merchants, PSPs, and financial institutions.

1. Purpose and Structure:

Fees are generally flat charges levied for specific services. For example, a payment gateway might charge a fixed monthly fee for access to its services, regardless of the number of transactions processed. In contrast, commissions are typically percentage-based and are earned as a reward for facilitating transactions or services. For instance, an acquiring bank earns a commission (part of the MDR) each time it processes a payment for a merchant.

2. Calculation Method:

Fees are usually predetermined and not dependent on transaction volume or value. Commissions, however, are often variable, depending on factors like transaction value, type of payment method, or the specific agreement between the parties involved.

3. Application and Impact:

Fees are applied as a cost for using a service, such as maintenance fees for an account or withdrawal fees at ATMs. They impact the overall cost structure of businesses and consumers alike. Commissions, on the other hand, serve as an incentive for intermediaries to facilitate transactions. For example, interchange commissions incentivize card-issuing banks to promote the use of their cards.

4.Revenue Models:

For many financial institutions and PSPs, fees constitute a stable, predictable revenue stream. Commissions, however, are more dynamic and tied to transaction volume and value, making them less predictable but potentially more lucrative.

The Future of Commissions in the Payment Ecosystem

As we move further into the growing digital age, the landscape of commissions is likely to evolve.

- Dynamic Pricing Models: With advancements in technology, we might see more dynamic pricing models where commissions fluctuate based on transaction size, volume, or even the time of day.

- New Payment Methods: Emerging payment methods such as cryptocurrency could introduce new types of commissions or even eliminate them altogether, disrupting the traditional payment ecosystem.

- Regulatory Changes: Governments around the world are increasingly scrutinizing interchange fees and other commissions, which could lead to regulatory changes that impact how these fees are structured.

Conclusion

Understanding commissions in the payment ecosystem is not just about knowing the costs; it's about gaining the upper hand in financial strategy. For organizations, a deep understanding of these commissions and fees empowers them to negotiate better rates with payment processors, potentially saving significant amounts of money. It allows businesses to assess the various options available, ensuring they choose the most cost-effective payment processors that align with their financial goals.

Additionally, by re-evaluating payment methods, companies can optimize their payment processes, avoiding unnecessary fees and improving overall efficiency. This strategic approach can lead to substantial savings, which can be reinvested into the business to drive growth. On the other hand, customers should also be aware of these fees as they often influence the prices of goods and services.

When consumers understand the impact of commissions on pricing, they can make more informed decisions, potentially seeking out vendors who offer better value by minimizing these hidden costs. In a rapidly evolving payments landscape, staying informed about how commissions work is essential for both businesses and customers to navigate the marketplace effectively and make financially sound decisions.

To simplify commission tracking and manage complex payment data more efficiently, businesses can also leverage modern financial technology solutions. Optimus Fintech helps organizations streamline payment reconciliation, gain better visibility into transaction commissions, and improve overall payment ecosystem management.

FAQs

What is a payment ecosystem?

It starts with a simple tap—someone pays. Behind it, banks, processors, and tech platforms move in sync. A payment ecosystem is this network that keeps money flowing smoothly and securely.

How do commissions work in the payment ecosystem?

Every payment carries a small fee. It’s split between banks, gateways, and service providers. Each takes a share for keeping the system running.

Why do banks charge commissions on financial transactions?

Moving money isn’t free. Banks maintain systems, security, and compliance checks. Commissions help cover these costs and keep transactions reliable.

What factors influence commission charges in payment transactions?

Not all payments are the same. Fees depend on the method, transaction size, volume, and agreements. It shifts—but always with a reason.

Why are commissions important in the digital payment industry?

They keep the ecosystem alive. Every player gets paid for their role. And in return, payments stay fast, secure, and seamless.